insight

AAM Corporate Credit View: Summer 2014

July 11, 2014

[toc]

AAM hosted its biannual client conference last month. A popular question was “Is corporate credit overvalued?” To benefit those who missed the conference, we decided to share our answer in this quarter’s AAM Corporate Credit View as well as how we are positioned for the risks ahead.

Corporate Credit Continued to Perform Well in the Second Quarter

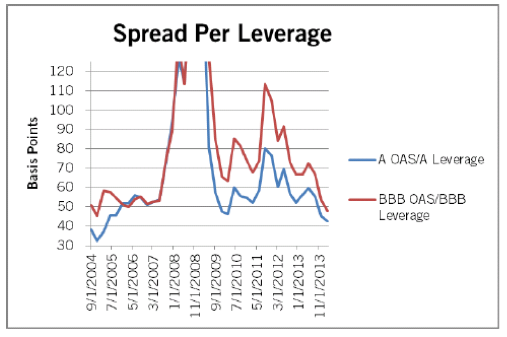

Corporate credit spreads tightened 7 basis points (bps) in the second quarter, supported by dovish comments from the Federal Open Market Committee (FOMC), constructive domestic economic data, and persistent low market volatility. Similar to the first quarter, the Investment Grade corporate market generated 2.8% total return (0.66% excess return) in the second quarter, as represented by the Barclays Corporate Index. BBB rated securities generally outperformed, narrowing the basis between A rated Industrial securities from 60 bps at year-end 2013 to 44 bps. Comparing credit spreads to credit fundamentals such as leverage over time, we consider BBB rated securities fairly valued (Exhibit 1). Moreover, spread volatility has been minimal (6 bps YTD), thus OAS-to-spread volatility remains above average. We expect this low level of volatility to persist for the next quarter, which is supportive for spreads.

Exhibit 1: Spreads have tightened while leverage has increased

Source: Barclays, CapitalIQ, AAM

Market Technicals Remain Supportive for Spreads

Demand remains very strong for Investment Grade securities. The secondary market continued to benefit from positive fund flows, and new issues remained oversubscribed with little concession versus outstanding securities. We are starting to see an increasing number of infrequent issuers with more credit risk (e.g., small REITs, Baidu) issue debt at negative concessions to their secondary spreads. And, issuers are taking advantage of investors’ quest for yield by issuing 50 year debt with minimal additional spread.

Long end maturities performed better in the second quarter, but intermediate (7-10 year) debt continued to outperform. Importantly, JP Morgan revised its forecast for fixed income supply down from $712 billion to $562 billion (vs. 2013’s actual of $864 billion) due mainly to lower supply of structured products and high yield. Investment Grade corporate supply is tracking ahead of forecast, but issuance in the second half may underwhelm if companies pushed forward their issuance due to lower than expected rates. Issuance to fund mergers and acquisitions (M&A) is increasing, and we expect this to support the level of issuance next year. However, outside of Investment Grade corporates, we do not expect issuance in other fixed income sectors to materially increase. This strong technical is driving spreads and should remain supportive for corporate credit.

Economic Growth Remains Muted

Economic data improved in the second quarter but remained in line with expectations. Given inflation targets set by the European Central Bank and the Bank of Japan, we could be entering a period when the U.S. is tightening monetary policy while Europe and Japan are easing. This has implications for the U.S. Dollar and thus, commodity prices. China remains committed to its GDP target of 7% and continues to be accommodative. We believe it will be difficult for U.S. GDP growth to exceed 3%, as consumers feel the effects of rising gasoline and electricity prices along with rising food and rent costs.

We Expect Management Teams to Pursue Mergers & Acquisitions and Add Leverage to Boost ROE

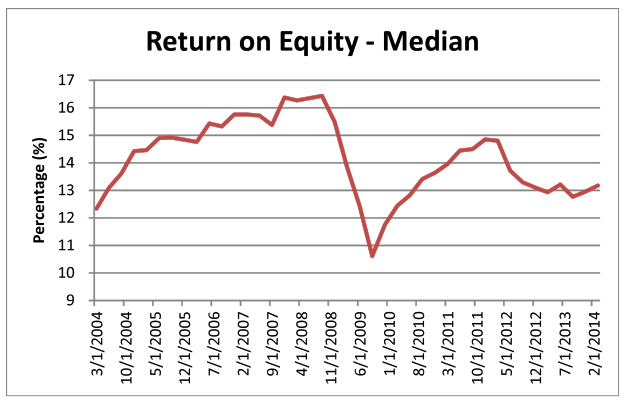

Little has changed in credit fundamentals in the second quarter except for management teams’ willingness to pursue M&A. Return on equity (ROE) has fallen post crisis (Exhibit 2) despite increasing margins, debt leverage, and share repurchases due to the low level of revenue growth. Revenue growth for the median firm is approximately 2 percentage points lower than it was before the recession. As you would expect, firms get more aggressive in the latter part of the credit cycle, willing to accept financial risk and stretching to produce the returns shareholders expect. In 2007, M&A deal volume was high and few deals were equity financed. Year-to-date, the dollar volume of deals financed with stock is high due to the very large deals that have been announced. But, on a deal volume basis, it doesn’t look as favorable with a high proportion funded with debt and/or cash. Our expectation is for the number of deals to increase and financing to be more cash based.

Exhibit 2: ROE continues to fall

Source: AAM, Capital IQ (Universe includes 435 Industrial companies

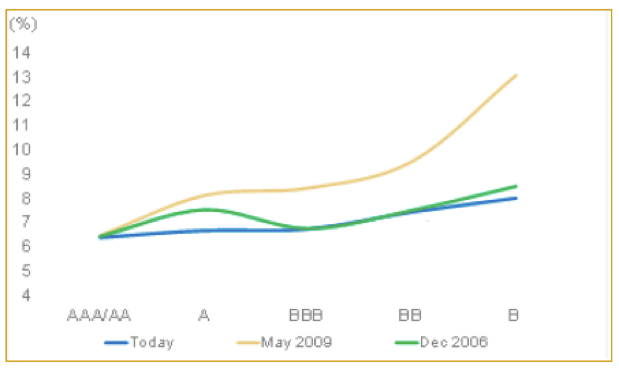

We believe event risk will be the main contributor to credit rating downgrades and spread widening over the next 12 to 24 months. We expect the downgrades to mainly come from companies leaving the single-A category, moving into the BBB-category, as there is little difference from a cost of capital standpoint (Exhibit 3), and companies continue to have access to the Investment Grade market. While that is not great for performance for that particular issuer, with the potential for prices to fall 1-6%, we believe it will remain relatively contained.

Exhibit 3: Weighted Average Cost of Capital (WACC) curve is relatively flat

Source: Morgan Stanley, Yieldbook, Bloomberg

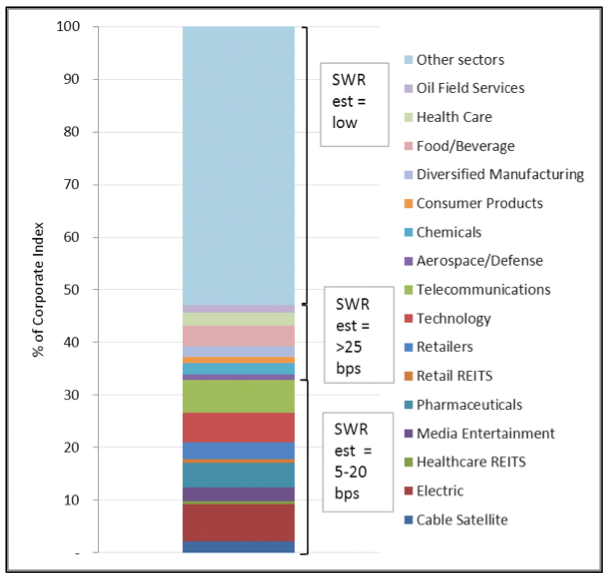

The sectors listed in Exhibit 4, we believe are more vulnerable to event risk (e.g., M&A, increasing leverage) and the commensurate degree of spread widening. Assuming we are correct with the projected spread widening, we would still expect the market to generate modestly positive excess returns, as the income associated with 55% of the market that is not vulnerable to event risk offsets the spread widening of the sectors below.

Exhibit 4: Spread Widening Risk is Higher in Growth Challenged Sectors

Source: Barclays, AAM; SWR = Spread widening risk; est = estimate)

Regulatory Oversight Should Prevent a Large LBO

What would be detrimental to the Investment Grade market is a large leveraged buyout (LBO). While we would not be surprised to see select LBOs like we did last year, we are not expecting a large deal like we saw in 2006-2007 because of increased regulatory involvement. Regulators are not allowing the banks to underwrite secured loans with more than six times debt to earnings because they do not believe it is good for the economy. And, while nonbank financial institutions are happy to pick up that business, they don’t have the balance sheets to fund large deals (>$20 billion).

Spreads are Fully Valued but Reflect The Cost of Liquidity and Credit Loss

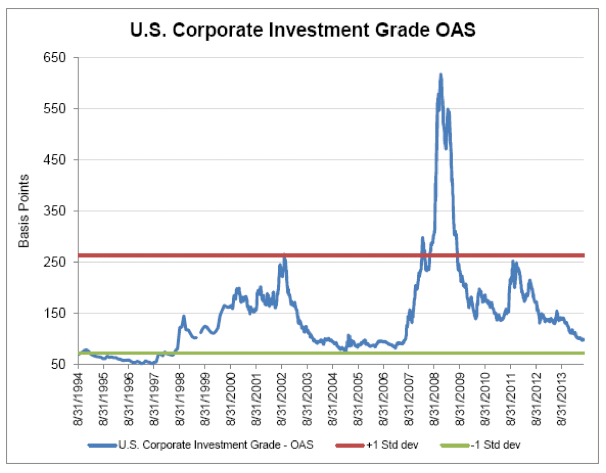

Exhibit 5: OAS remains within one standard deviation of its 20 year mean

Source: Barclays, AAM

We recognize that spreads are at the low end of the range historically (Exhibit 5). This reflects the lower level of systemic risk and uncertainty and the very strong technical bid with fixed income supply half its pre-crisis level. Corporate default rates are expected to remain low over the near term. Citigroup’s strategist states that using the worst 10 year default period for credit and a 40% recovery assumption, the data suggests High Grade bond spreads would be just 32 bps. That assumes they only reflect expected losses from defaults. Of course they should be wider because of other risks such as liquidity, which has increased post financial crisis. We estimate the cost of market liquidity to be approximately 35 bps, bringing the OAS floor to 67 bps. This compares to a market OAS at June 30, 2014 of 99 bps. The additional 32 bps is

We recognize that spreads are at the low end of the range historically (Exhibit 5). This reflects the lower level of systemic risk and uncertainty and the very strong technical bid with fixed income supply half its pre-crisis level. Corporate default rates are expected to remain low over the near term. Citigroup’s strategist states that using the worst 10 year default period for credit and a 40% recovery assumption, the data suggests High Grade bond spreads would be just 32 bps. That assumes they only reflect expected losses from defaults. Of course they should be wider because of other risks such as liquidity, which has increased post financial crisis. We estimate the cost of market liquidity to be approximately 35 bps, bringing the OAS floor to 67 bps. This compares to a market OAS at June 30, 2014 of 99 bps. The additional 32 bps is compensating investors for volatility, which given a market duration of 7, assumes it falls 1 bps from the current level[note]Note: We are assuming investors require sufficient income to compensate for a one standard deviation move in OAS. Therefore, a market duration of 7 and OAS standard deviation of 5 would require 35 bps of spread to break even over 12 months if OAS widened one standard deviation. The same applies to the cost of liquidity. The bid ask spread is 5 bps on average, and given a duration of 7, investors would need 35 bps of income to offset this cost over a 12 month timeframe.[/note]. We believe this is a reasonable assumption given where we are in the credit cycle (Exhibit 6), but it leaves little room for further spread tightening.

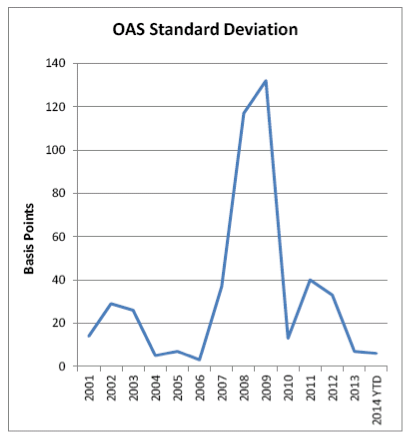

Exhibit 6: Standard deviation is expected to remain low over the near term

Source: Barclays, AAM

Position the Portfolio Defensively, Using Credit and Sector Selection

In conclusion, over the near term, we expect spreads to stay in this narrow band. The downside risks that would likely result in spread widening include a sudden move in rates, an exogenous shock, or a large LBO. Upside risks include better economic data or unexpected deleveraging by companies. Market technicals are benefitting spreads and are likely to continue to do so over the near term. Credit quality is good today and systemic risk is low, and even though spreads are tight, they are wide of the cost of liquidity and loss given default and compensate investors for the expected low level of volatility. We are not recommending portfolio managers upgrade the quality of their portfolios because we expect more ratings migration down from A to BBB than we do from BBB to BB. Case in point, after a failed merger with Syngenta, Monsanto decided to increase its leverage, resulting in ratings falling from A1/A+ to A3/BBB+. Monsanto’s spreads widened more than 25 bps. We believe it’s more prudent to be selective or defensive in this environment, not bearish.

Private Placement Market Update

We have participated in the private placement market in the first half of 2014. Currently, we are seeing frothiness in that market as well as project loans. The grab for yield has resulted in aggressive pricing and terms with investor demand outpacing supply. Volume is tracking lower than 2013, as issuers are increasingly accessing the European corporate market after the spread tightening that has materialized over the last couple of years. Therefore, we are investing selectively in this asset class as well.

For more information about AAM or any of the information in the Corporate Credit View, please contact:

Colin Dowdall, CFA, Director of Marketing and Business Development

John Olvany, Vice President of Business Development

Neelm Hameer, Vice President of Business Development

Disclaimer: Asset Allocation & Management Company, LLC (AAM) is an investment adviser registered with the Securities and Exchange Commission, specializing in fixed-income asset management services for insurance companies. This information was developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as “AAM”), and their representative officers and employees. This report has been prepared for informational purposes only and does not purport to represent a complete analysis of any security, company or industry discussed. Any opinions and/or recommendations expressed are subject to change without notice and should be considered only as part of a diversified portfolio. A complete list of investment recommendations made during the past year is available upon request. Past performance is not an indication of future returns.

This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, inflation, liquidity, valuation, volatility, prepayment and extension. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.

Disclaimer: Asset Allocation & Management Company, LLC (AAM) is an investment adviser registered with the Securities and Exchange Commission, specializing in fixed-income asset management services for insurance companies. Registration does not imply a certain level of skill or training. This information was developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as “AAM”), and their representative officers and employees. This report has been prepared for informational purposes only and does not purport to represent a complete analysis of any security, company or industry discussed. Any opinions and/or recommendations expressed are subject to change without notice and should be considered only as part of a diversified portfolio. Any opinions and statements contained herein of financial market trends based on market conditions constitute our judgment. This material may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different than that discussed here. The information presented, including any statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Although the assumptions underlying the forward-looking statements that may be contained herein are believed to be reasonable they can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. AAM assumes no duty to provide updates to any analysis contained herein. A complete list of investment recommendations made during the past year is available upon request. Past performance is not an indication of future returns. This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, inflation, liquidity, valuation, volatility, prepayment and extension. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.