FIRST QUARTER CORPORATE CREDIT UPDATE

Market Performance

The Investment Grade (IG) Corporate bond market reported very weak performance year-to-date (YTD) March 31, due mostly to rising interest rates.* That said, spreads versus Treasuries increased to reflect the uncertainties related to inflation and the Federal Reserve’s ability to navigate. The IG market generated an excess return versus a duration neutral Treasury of -1.5%, and when including the underlying Treasuries, the total return YTD was -7.7%. The increase in yield has resulted in close to 25% of the IG market priced below $90, and that percentage increases to 70% if one narrows the universe to 30+ year bonds.* This performance compares to the S&P Index returning -4.6% and the High Yield market returning -4.8% (per Bloomberg Barclays) during the same period.

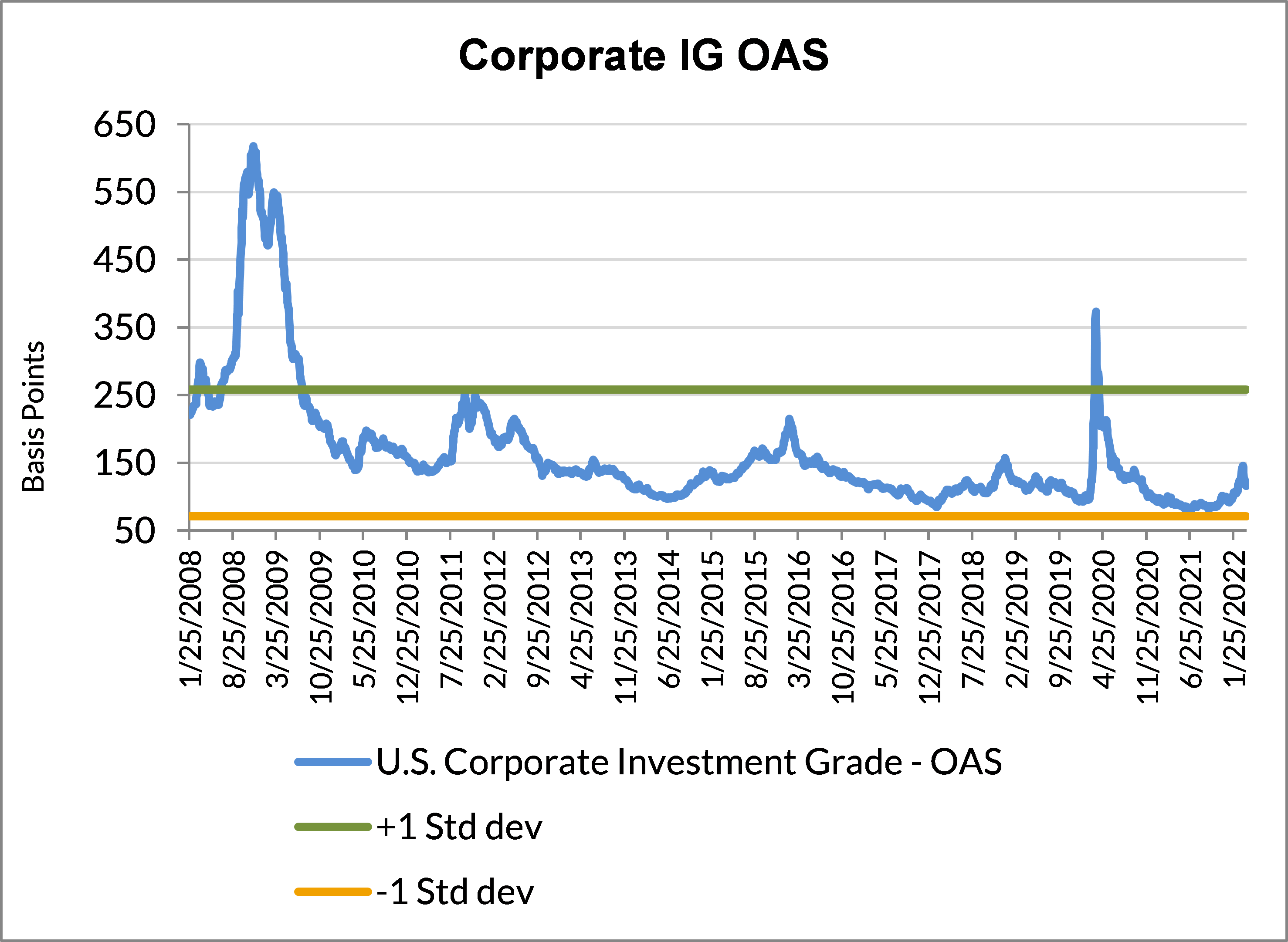

The option adjusted spread (OAS) of the IG market widened 24 basis points (bps) to 116, with long maturities and ‘BBB’ rated bonds underperforming. The differential between ‘A-/higher’ and ‘BBB’ rated bonds widened 12 bps to 57, very close to the 3-year median of 59.* Lacking technical support, intermediate bond spreads have widened more than short and long bonds. As one would expect in this environment given their fundamental support, commodity-based sectors have outperformed. Financials have underperformed mostly due to a higher than expected debt issued in 2022. We believe all measures are consistent with positive economic growth and are not communicating that a recession is imminent.

Exhibit 1: Corporate IG OAS has returned to Fair Value

Fundamentals

After a year of strong EBITDA growth and debt reduction in 2021, companies’ balance sheets seem to be in good shape. According to AAM’s analysis, commodity and cyclical firms have reduced debt leverage to 7+ year lows. Defensive sectors have also reduced leverage to pre-pandemic levels.

According to information provided by FactSet, equity analyst estimates for this year appear optimistic, with stable-to-expanding margins and double-digit EBITDA growth. The war and the Federal Reserve’s more aggressive stance on inflation have likely increased the uncertainty of these estimates. While we expect first quarter results will be good, we believe second half 2022 estimates are at risk. This is likely to put pressure on the equity market. Positively for the economy, capital spending is expected to be strong this year, and we expect little modification. Generally, companies are investing in new technology and processes as well as investments related to ESG.

Liquidity

After a period of monetary and fiscal stimulus, corporate and consumer balance sheets seem to be healthy, and there is cash waiting to be deployed in private debt and equity markets. That is very supportive for not only the economy but default risk as well. There has been strong demand for new issue corporate IG debt, and loan demand remains solid as reported by U.S. banks. Financial conditions are mixed depending on the measure, but banks continue to report favorable lending standards.

The amount of negative yielding debt globally has quickly fallen as yields have risen, which helps savers and lenders across the globe. In the near term, we don’t expect more fiscal stimulus, and we believe the Federal Reserve will fight inflation first. Except for yield related buying, technicals in the IG market have not been as supportive this year, with negative fund flows, increasing hedging costs for foreign investors, and higher than expected new issue supply. Looking ahead, we expect hedging costs to remain burdensome, but new issue supply to slow and yield buyers to remain.

Market Outlook

Recession is not AAM’s base case, but our economic forecast has been tempered. Accordingly, we expect performance will be more idiosyncratic and markets more volatile. It will likely be another challenging year for many management teams. Europe is at risk economically with the war, increasing uncertainty for companies at a time when they were already dealing with a sluggish re-opening after Covid, elevated energy prices and supply chain challenges. We would expect financial conditions to tighten in Europe as a result of this uncertainty. In the U.S., we expect consumers to be less active as real incomes fall. We are starting to see recession-like shopping behavior (e.g., trading-down), cautiousness in discretionary spending by large companies (e.g., national advertising cancellations) and a loss in small business confidence as measured by the NFIB. We are taking a closer look at companies with outsized exposures to these markets/issues.

By nature, fixed income investors worry about the recession around the corner. Our less favorable economic outlook and expectation for increased volatility has resulted in a widening of our expected range for OAS at yearend 2022. We expect OAS to remain mostly rangebound around 100-135 with levels outside of that considered rich or attractive. Sectors such as Energy, and Wirelines have outperformed this year, as spreads were attractive at the start of the year, and have outperformed as the market has rewarded firms with favorable (and possibly more certain) fundamental outlooks.* We see value in sectors that have been pressured from higher levels of debt supply, such as Banks. We see less attractive risk adjusted income in sectors such as Media, Consumer Products, and Life Insurance. While our insurance portfolios are overweight corporate bonds, we are more defensive in our curve and sector positioning, and we have invested in companies we believe will outperform in this environment. We continue to favor the new issue market, which is offering attractive concessions versus secondary bonds.

* Source: Bloomberg Barclays Corporate Index

Disclaimer: Asset Allocation & Management Company, LLC (AAM) is an investment adviser registered with the Securities and Exchange Commission, specializing in fixed-income asset management services for insurance companies. Registration does not imply a certain level of skill or training. This information was developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as “AAM”), and their representative officers and employees. This report has been prepared for informational purposes only and does not purport to represent a complete analysis of any security, company or industry discussed. Any opinions and/or recommendations expressed are subject to change without notice and should be considered only as part of a diversified portfolio. Any opinions and statements contained herein of financial market trends based on market conditions constitute our judgment. This material may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different than that discussed here. The information presented, including any statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Although the assumptions underlying the forward-looking statements that may be contained herein are believed to be reasonable they can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. AAM assumes no duty to provide updates to any analysis contained herein. A complete list of investment recommendations made during the past year is available upon request. Past performance is not an indication of future returns. This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, inflation, liquidity, valuation, volatility, prepayment and extension. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.