insight

The Great Bank Reversal of 2016

March 10, 2016

The Bank sector has experienced a reversal of its strong relative performance vs. the Corporate Index during the first quarter of 2016. In this white paper, AAM’s bank analyst examines the drivers of performance in the sector and looks at trades that have outperformed during the recent volatility.

In fiscal year 2015, the Bank sector was one of the best performing subsectors of the Barclays Capital U.S. Corporate Investment Grade Index (“the Index”), reflecting strong capital, improving asset quality and expectations of an impending rate hike cycle.

This trend reversed abruptly in the first two months of 2016 with banks participating in the sharp acceleration of negative excess returns in the Index. As of February month end, the bank sector had generated year-to-date negative excess returns of -227 basis points (bps) as compared to -248 bps for the Index. While broad corporate bond performance has retraced some of this performance in March, the bank sector has actually lagged the overall Index, having generated 40 bps of positive excess returns month-to-date vs. 94 bps for the Index.

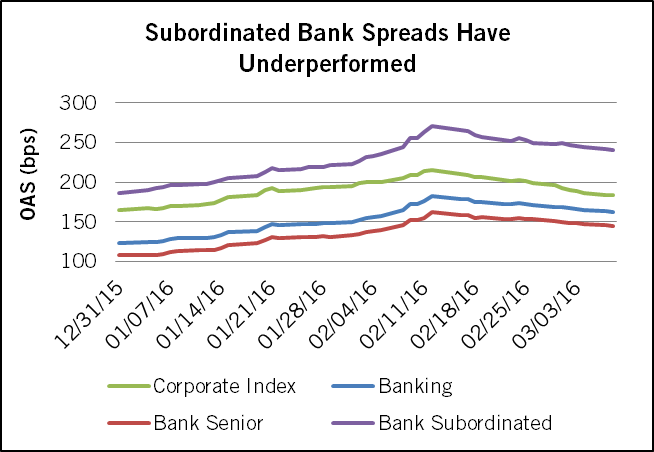

However, a more granular examination of the performance in the bank sector better illustrates what trades have helped or hurt performance in the space. If we break out performance of senior bank bonds vs. subordinated bonds (the latter representing the riskier portion of the bank capital structure), it quickly becomes clear that the bulk of the negative excess returns were driven by the subordinated bonds (-498 bps through February). In contrast, senior bank bonds actually outperformed the Index with negative excess returns of -163 bps through February (Exhibit 1).

Exhibit 1:

Source: Barclays, AAM

Additionally, the performance in the bank sector has been depressed by the non-domestic (Yankee) banks (-203 bps excess returns YTD for Yankee banks vs. -186 bps for banks overall). The negative performance in Yankee banks was driven in particular by the sharp sell-off in European banks in February as fears about capital adequacy and the ability to continue paying coupons on capital securities were sparked by poor financial results and diminished return on equity prospects for several of the continent’s largest banks (Deutsche Bank, Credit Suisse and Unicredit were all subject to material sell-offs).

Anecdotally, many total return managers were also hurt by their overweighting of Additional Tier 1 /Contingent Convertible (CoCo) securities, which represents an investment in the most junior layer of the bank capital structure. While CoCos are not included in the Index (because they are generally not investment grade rated), they generated very strong performance in fiscal year 2015 (+6.3% total return), and were a top recommendation of most sell-side credit strategists heading into 2016. However, through February AT1/CoCos delivered a -8.6% total return as fears about coupon sustainability grew.

So how is AAM positioned within the bank space?

We have been overweight the bank sector since mid-2009 based on improving fundamentals and an increasingly benign economic outlook. However, within the bank sector we have retained a strong preference for senior vs. subordinated bonds, reflecting a preference for downside protection and a desire for clarity on Total Loss Absorbing Capacity/Capital (TLAC) rules. We have also increasingly weighted regional and community banks vs. universal banks, reflecting the potential for increased issuance by universal banks to meet TLAC minimum debt requirements, as well as our view that the traditional banking model of the regional space was likely to have better fundamental momentum in a slow growth environment and less residual regulatory liability.

Finally, we have been underweight Yankee banks, and particularly European banks, since macro-political instability in Greece, Italy and Spain sparked the European sovereign crisis in 2011. Although fears of a Euro or EU break-up have receded somewhat, we have remained underweight as we feel the underlying causes of that crisis (lack of political consensus and stagnant economic growth) remain unresolved. Additionally, we view the European universal banks as having a much greater restructuring burden with regard to meeting TLAC requirements as compared to the U.S. universal banks.

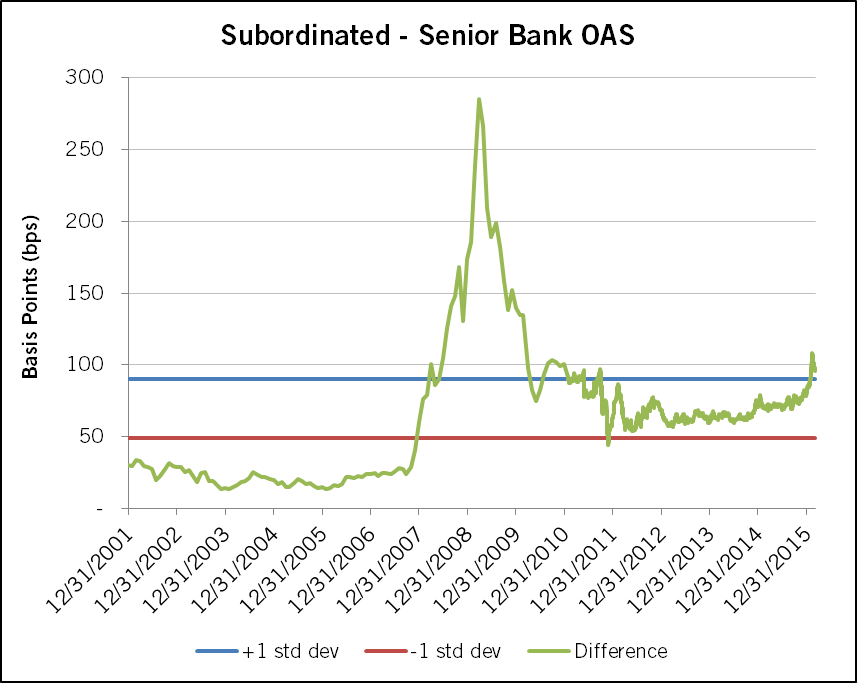

While our underweight to subordinated debt and Yankee banks constrained investment performance during 2014 and 2015, the benefits of this credit selection can be seen in the downside protection in periods such as the first quarter of 2016. Conversely, we began selectively investing in subordinated bank debt of the U.S. universal banks in late February, as we felt that the spread widening over the previous two months had made certain credits attractive given our fundamental outlook (Exhibit 2).

Exhibit 2:

Source: Barclays, AAM

Written by:

N. Sebastian Bacchus, CFA

Senior Analyst, Corporate Credit

For more information, contact:

Colin T. Dowdall, CFA

Director of Marketing and Business Development

colin.dowdall@aamcompany.com

John Olvany

Vice President of Business Development

john.olvany@aamcompany.com

Neelm Hameer

Vice President of Business Development

neelm.hameer@aamcompany.com

Disclaimer: Asset Allocation & Management Company, LLC (AAM) is an investment adviser registered with the Securities and Exchange Commission, specializing in fixed-income asset management services for insurance companies. Registration does not imply a certain level of skill or training. This information was developed using publicly available information, internally developed data and outside sources believed to be reliable. While all reasonable care has been taken to ensure that the facts stated and the opinions given are accurate, complete and reasonable, liability is expressly disclaimed by AAM and any affiliates (collectively known as “AAM”), and their representative officers and employees. This report has been prepared for informational purposes only and does not purport to represent a complete analysis of any security, company or industry discussed. Any opinions and/or recommendations expressed are subject to change without notice and should be considered only as part of a diversified portfolio. Any opinions and statements contained herein of financial market trends based on market conditions constitute our judgment. This material may contain projections or other forward-looking statements regarding future events, targets or expectations, and is only current as of the date indicated. There is no assurance that such events or targets will be achieved, and may be significantly different than that discussed here. The information presented, including any statements concerning financial market trends, is based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Although the assumptions underlying the forward-looking statements that may be contained herein are believed to be reasonable they can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. AAM assumes no duty to provide updates to any analysis contained herein. A complete list of investment recommendations made during the past year is available upon request. Past performance is not an indication of future returns. This information is distributed to recipients including AAM, any of which may have acted on the basis of the information, or may have an ownership interest in securities to which the information relates. It may also be distributed to clients of AAM, as well as to other recipients with whom no such client relationship exists. Providing this information does not, in and of itself, constitute a recommendation by AAM, nor does it imply that the purchase or sale of any security is suitable for the recipient. Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, inflation, liquidity, valuation, volatility, prepayment and extension. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission.