Recap

During the first half of the year, the municipal market has weathered a substantial amount of volatility in the wake of the COVID-19 pandemic and the resulting shut-in orders across the country. For tax-exempts, in reviewing data published by Municipal Market Data (MMD), 10yr AAA muni-to-Treasury ratios reached a record 354% at the most severe point of the market dislocation on March 10th. On a tax-adjusted basis using the 21% corporate tax rate, that high point in ratios resulted in muni spreads to Treasuries to hit 256 basis points (bps). These relative value metrics started the year at 75% and -19bps, respectively. Taxable munis, however, were far more resilient, with 10yr AAA spreads to Treasuries widening by 114bps to 168bps on April 10th, using market data compiled by AAM.

Market Recovery

Since the worst of the market dislocations, both muni sectors have improved substantially during the 2nd quarter due to policy responses to the pandemic. State and local governments received federal stimulus of ~$235 billion from the CARES Act, with $150 billion of that aid narrowly focused towards COVID-related expenses. Additionally, the CARES Act provided funding for the Municipal Liquidity Facility (MLF) through the Federal Reserve, which provides loans to eligible municipalities. Although this support is not deemed sufficient to mitigate the budget stress from the projected estimates of $500 billion in revenues losses for state and local governments for fiscal 2020 and 2021, the support seemed to be enough to assuage the concerns that massive defaults could develop during the recession.

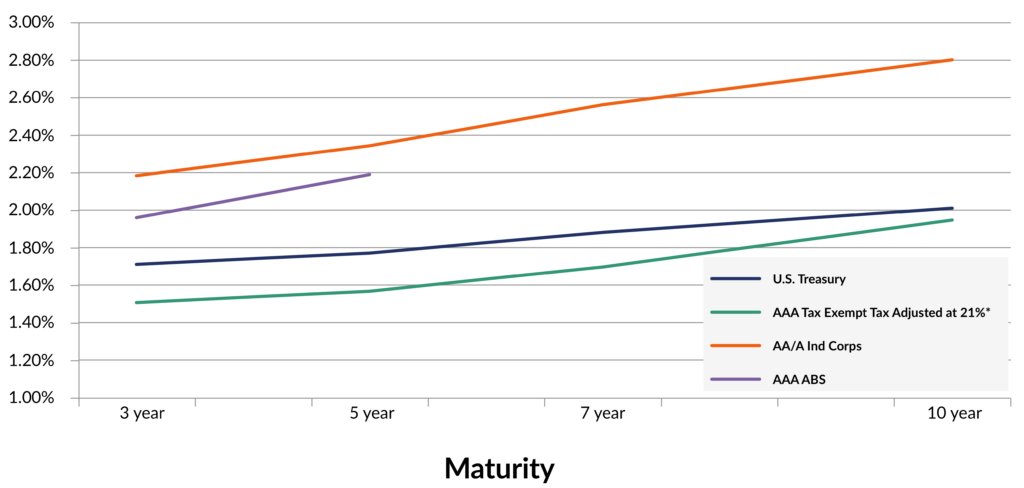

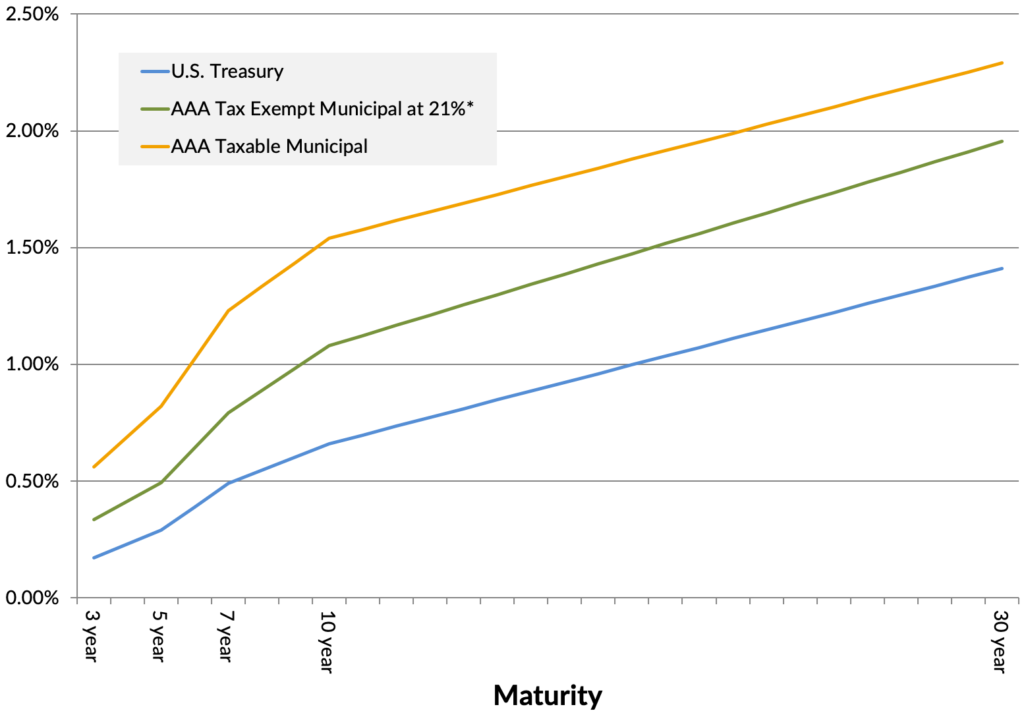

The more constructive, albeit cautious, tone in the market resulted in stronger demand, which helped drive relative valuations to stronger levels to end the 2nd quarter. As shown in Exhibit 1, for tax-exempts, AAA muni-to-Treasury ratios in 10yrs would end the quarter at 137%. On a tax-adjusted basis (21% corporate rate), yield spreads in 10yrs would tighten by 213bps from their wide point to end the quarter at 42bps.

Taxable munis also saw very strong performance. From their widest points during the quarter, spreads for AAA’s have contracted by 80bps. Per the graph in Exhibit 1, spreads to end the quarter were at 88bps (i.e., 46bps wider than tax-exempts on a tax-adjusted basis). For insurance companies taxed at 21%, we view this level as attractive and a compelling entry point to add exposure to the basis.

Exhibit 1: Market Yield as of 7/1/2020

Compelling Spread Tightening Potential for Taxable Munis

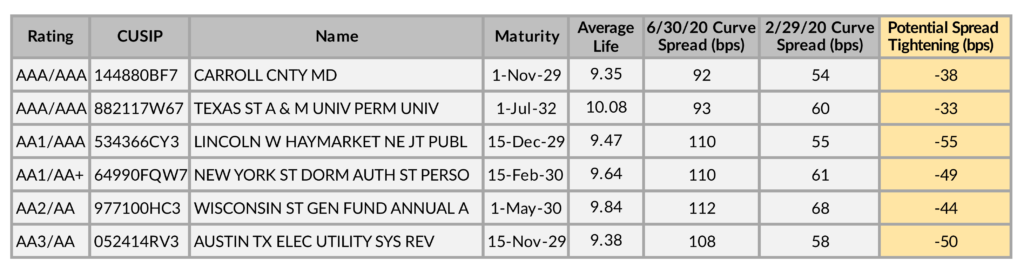

Although the taxable muni sector has generally exhibited extraordinarily strong demand over the last quarter, spread levels still appear to be a long way off from their pre-COVID trading levels. In the following table (Exhibit 2), we compiled and reviewed the market evaluation levels for representative, liquid issuers across the AAA and AA ratings categories. The listed examples compare issuer yield spreads (i.e., to the interpolated Treasury yield curve) from the end of February to the spread levels for those issuers at the end of the 2nd quarter. For the AAA category, there appears to be an additional 33 to 38bps of additional spread tightening before we capture a full normalization towards pre-COVID trading levels. For the AA category, potential tightening is an even more compelling 44 to 55bps. We find that because of the expected heavy supply of taxable munis this year and its heavy concentration of issuance in the 10 to 20yr maturity range, that this area of the yield curve provides the best value proposition.

Exhibit 2: Potential Spread Normalization to Pre-COVID Levels

Outlook: Supply Surge Should Provide Ample Opportunities to Add Exposure

As states have come to terms with the new realities of their fiscal condition and as they move aggressively to correct structural imbalances, every tool available to issuers is expected to be utilized. Municipalities have already started laying off employees, reducing services, postponing or cancelling capital spending plans and engaging in deficit financing. With the dramatic drop in Treasury yield levels this year from the Federal Reserve’s substantial easing in monetary policy, state and local governments are also expected to take full advantage of refinancing their debt to achieve substantial savings in debt service costs.

One of the primary tools towards that end will be to continue to utilize the issuance of taxable debt to refinance tax-exempt debt. At the end of 2017, tax reform under the Tax Cut and Jobs Act (TCJA) eliminated the use of tax-exempt advance refundings. Prior to the TCJA, this process allowed for the refinancing of tax-exempt debt more than 90 days before its call date, but under the new rules, the refinancing can now only be executed in the taxable municipal market. It was not until August of 2019 that Treasury rates were low enough to generate a substantial level of debt service savings to compel municipalities to aggressively utilize this refinancing technique. Based on data published by the Bond Buyer, taxable muni issuance between August 2019 to the end of the year was $50.5 billion, which was an increase of 209% versus the same period in 2018.

At the start of the year, Treasury yields remained low enough that the broker/dealer community estimated a total of between $95 to $120 billion of taxable muni issuance for 2020, most of which would be tied to taxable advance refundings. To put that number into perspective, according to published data from the Bond Buyer, average annual taxable municipal issuance over the last 8yrs has only been $36 billion per year. The pandemic-driven recession has helped push Treasury rates lower by another 126bps year-to-date, and combined with the recovery in taxable muni spreads during the 2nd quarter, interest savings under taxable advance refundings are even more compelling than they were at the beginning of the year. Consequently, we expect very heavy issuance of taxable municipals over the balance of the year, unless we see a dramatic turn in Treasury rates to higher levels.

While we view taxable municipals as an attractive sector and we are actively looking at adding exposure to the sector, we are aware that we could see the recent surge in COVID-19 cases lead to more downward pressure on state and local government revenues in the future. Consequently, we remain very cautious in our approach and plan to be very selective in the issuers that we target for investment, with an up-in-quality bias towards those issuers which have exhibited strong liquidity and budget flexibility metrics.