Market Recap

By Tim Senechalle, CFA

In AAM’s 2026 market outlook, our investment team highlighted the merits of selectivity and opportunism as we position client portfolios and deploy new capital. These priorities proved valuable in the 1st quarter as geopolitical developments, AI disruption, and private credit concerns were catalysts for volatility in rates, credit, and equity markets. Among the notable shifts:

• 10-year U.S. Treasury notes traded across a 50 basis points range1

• Investment grade corporate bond spreads widened 22 basis points relative to January lows2

• Stock prices fell with dramatic dispersion of total returns as Energy Sector shares gained 37% while Information Technology shares declined 9%3

Within the high grade market, which represents the majority of insurance investment portfolios, volatility provided attractive entry points to add quality securities at materially higher yields. We took advantage of compelling opportunities in new issue corporate bonds, ABS/CMBS secondaries, and Agency Residential MBS, which underperformed as rate volatility surged. Improved breadth of equity returns and heightened single-stock volatility benefited client portfolios with exposure to dividend focused shares or convertible securities, both of which materially outperformed large cap equity markets.

Sources: 1. Bloomberg 2. Bloomberg US Corporate Bond Index data 3. Standard & Poor’s Index GICS Level 1

Economic View

By Marco Bravo, CFA

Growth, the Treasury Curve, and the Fed

Heightened geopolitical tensions between the U.S., Israel, and Iran have added uncertainty to the outlook for inflation, consumer spending, and monetary policy. The recent surge in oil prices contributed to the largest month‑over‑month increase in headline CPI since mid‑2022, raising concerns that higher fuel costs could weigh on consumer spending, particularly among lower‑ and middle‑income households. This combination of renewed inflation pressure and emerging growth headwinds presents a challenge for the Federal Reserve as it balances price stability with slowing momentum in the broader economy.

Despite these risks, the U.S. economy entered the conflict on relatively solid footing. Continued gains in wages and household wealth should help support consumption, while AI‑related investment is expected to provide a meaningful boost to fixed investment. Increased tax refunds associated with the OBBB may offer an additional near‑term tailwind. Current forecasts point to approximately 2% GDP growth in 2026, though risks remain skewed to the downside. AAM views the probability of recession as low, contingent on a near‑term resolution to the conflict; a more prolonged or escalatory scenario would materially increase downside risks. Looking ahead, decelerating shelter costs should continue to support moderation in core inflation, though readings are likely to remain above the Federal Reserve’s 2% target. We expect the Fed to largely look through the oil‑price shock, focusing instead on labor‑market conditions and broader growth trends. With longer‑term inflation expectations well anchored, a rate cut later this year remains likely. The Treasury curve is expected to steepen modestly, with the 10‑year yield ending the year in a 3.9%–4.4% range.

Fixed Income Market

By Elizabeth Henderson, CFA

Fixed‑income markets navigated a mixed but resilient first quarter as shifting rate dynamics, heavy issuance, and geopolitical volatility drove performance. January began constructively on strong demand technicals, pushing investment‑grade corporate spreads to very tight levels and supporting securitized excess returns. February brought a reset as elevated supply, AI‑related sector repricing, and higher geopolitical risk widened corporate spreads despite continued inflows and active trading. Volatility intensified in March with rising Treasury yields, producing rate‑driven losses even as credit fundamentals remained generally sound; credits and structures linked to higher rates and commodity prices were relative winners. Sector dispersion increased overall, with corporates finishing wider after a round‑trip in excess returns, securitized assets proving more resilient, and municipals led results.

AAM Fixed Income Performance

By Elizabeth Henderson, CFA

Performance during the quarter was driven primarily by security selection, while sector allocation effects were largely offsetting. At a high level, overweights to securitized products and municipal bonds were balanced by underweights to U.S. Treasuries and an overweight to corporate credit. Security selection added meaningful value across portfolios, particularly in more specialized and less index‑heavy areas of the market, including community banks, non‑agency RMBS, esoteric ABS, single‑asset single‑property CMBS, and taxable municipal bonds. Analyst‑driven security selection was also additive in sectors with elevated idiosyncratic risk, including Technology and Consumer Non‑cyclicals. Areas of relative underperformance included an underweight to high‑coupon mortgages, reflecting their premium dollar prices and negative convexity in an environment where interest rates were expected to decline.

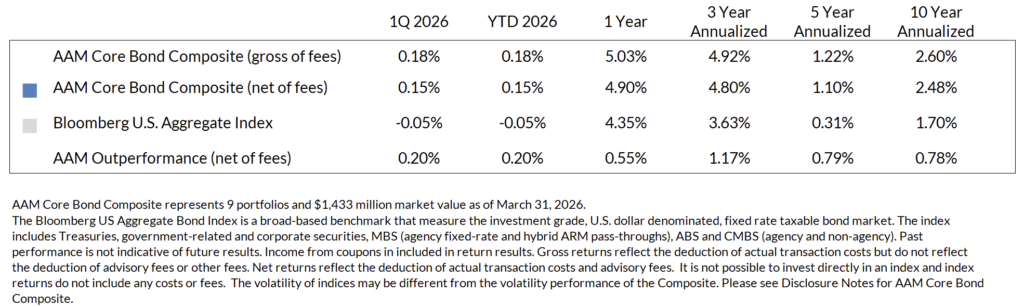

AAM Core Bond Composite

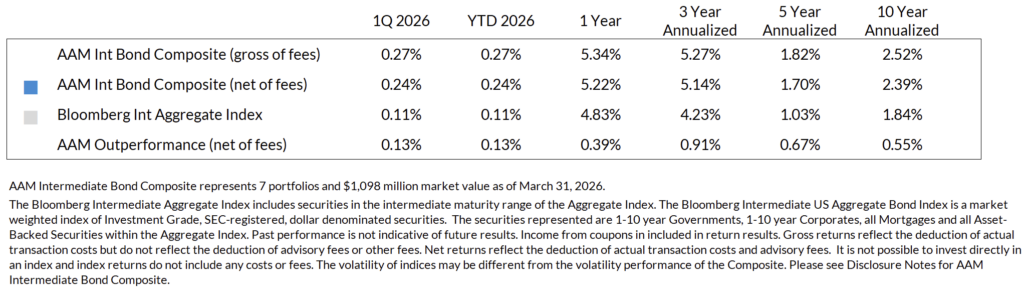

AAM Intermediate Bond Composite

Outlook for Insurance Portfolios

Public Fixed Income

The macroeconomic backdrop, which has investors expecting that the Federal Reserve ‘pause’ will remain in place for some time, has lifted benchmark yields and improved assumed reinvestment rates. New money yields for the insurance industry remain above industry book yields with accretive benefits to operating performance. As it relates to fixed income and our expectation for performance in the next quarter, we are positioning portfolios with yield and spread in the short end via esoteric ABS, CMBS, BBB Corporate bonds and Financials. We are comfortable with a modest exposure to floating rate instruments and high coupon mortgages, which should perform well in this environment over the next quarter. In the intermediate part of the curve, we prefer non-agency RMBS and new-issue corporate and taxable municipal bonds with additional spread at issuance vs. secondary offerings. Issuer selection for intermediate and longer duration bonds will continue to be a driver of performance given the increase in idiosyncratic risk and unfavorable break-evens in a spread widening environment. On the long end of the curve, we expect higher quality securities to outperform especially if the price of oil remains high and/or continues to climb, as risk premiums will need to increase and spreads on the long end are historically rich.

Expanding Beyond Public Markets: Opportunities and Risks

We are closely monitoring developments in two areas relevant to insurance investment portfolios. The first relates to evolving fundamentals and demand dynamics in private credit markets. In a whitepaper published in early April, our team wrote on this topic and highlighted the merits of diversification, credit research, value assessment, and structural integrity in these lesser liquid markets (Corporate Fundamentals 1Q26). We believe that institutional investors will benefit from opportunities brought about by undisciplined underwriting and unstable retail investor behavior and will deploy capital opportunistically in private markets for clients with an appetite for illiquid investments.

The second area relates to regulatory developments. The NAIC, other regulatory bodies, and rating agencies continue to focus on improved transparency around insurer investments and are actively seeking paths to mitigate investment risks to solvency. While regulatory capital efficiency is a valuable part of insurance strategy, an economic capital-centric investment process positions us to absorb the inevitable changes that follow market stresses and regulator responses. Stay tuned for a summary of upcoming regulatory developments from AAM’s insurance accounting and strategy team.

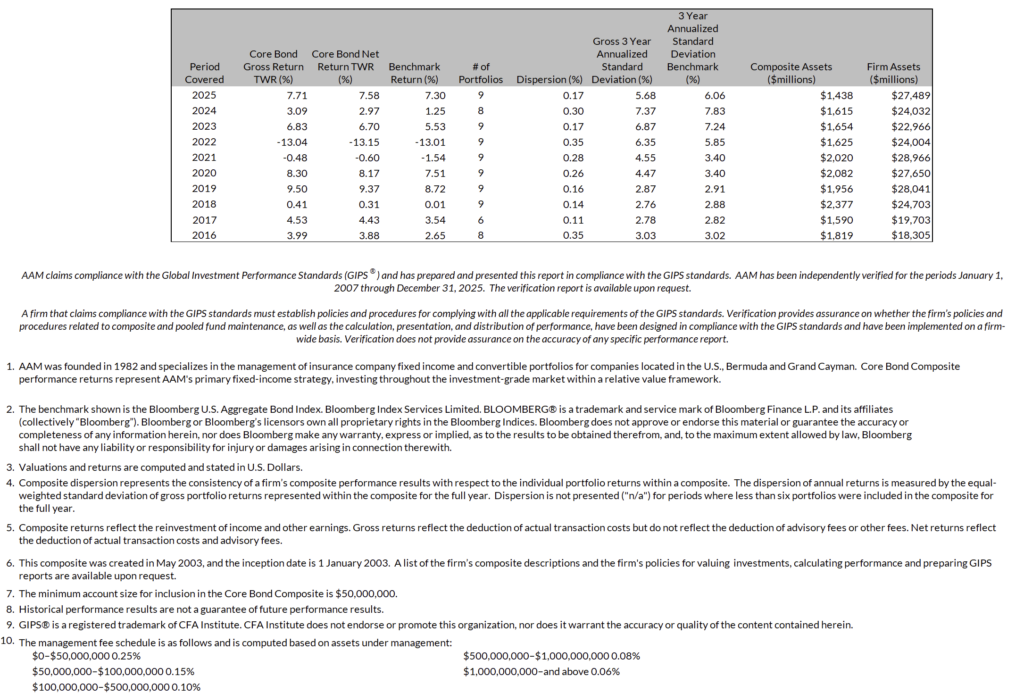

AAM Core Bond Disclosure Notes

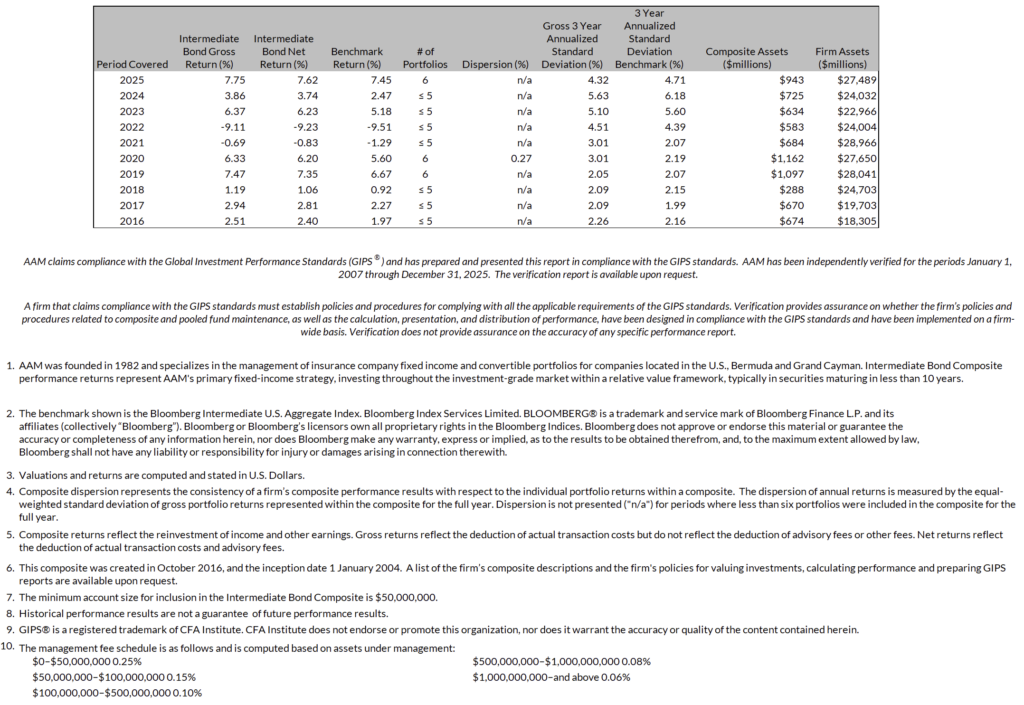

AAM Intermediate Bond Disclosure Notes

Corporate Fundamentals 2Q26; AI Debt Issuance Can’t Stop Won’t Stop

July 16, 2026