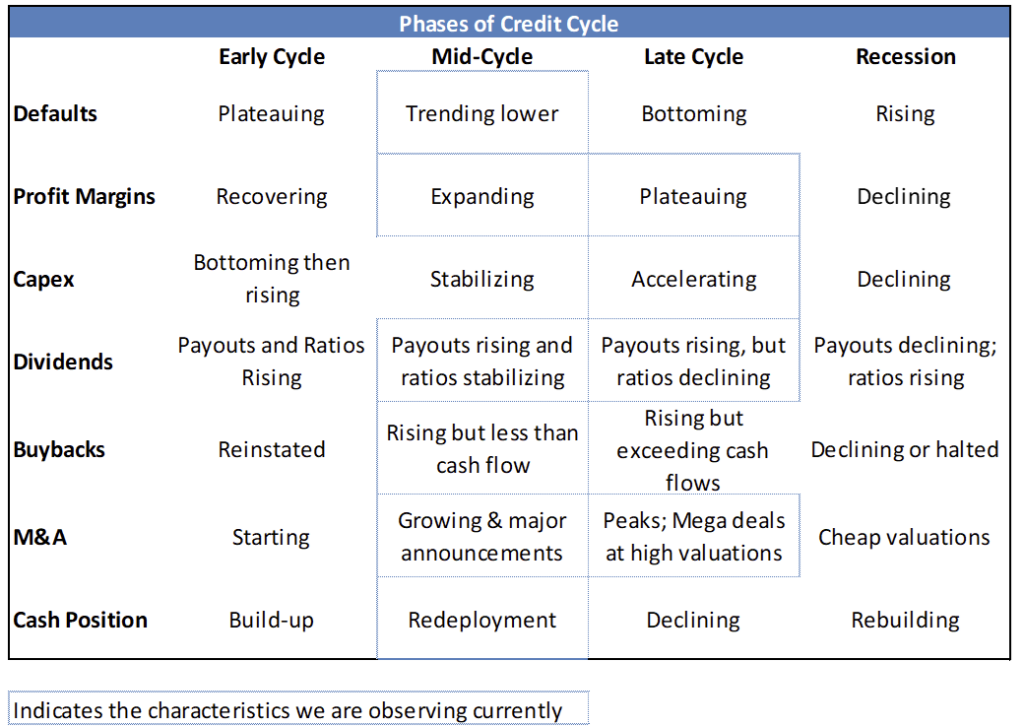

Volatility has risen 30% over the quarter driven by the conflict in the Middle East, the ongoing energy shock and escalating redemptions of private credit funds. Despite these issues, corporate fundamentals remain healthy and supportive of credit quality. Defaults are trending lower, profit margins are either expanding or stable, capital spending is accelerating, shareholder friendly activities are robust and internally funded while M&A is fairly active. These are characteristics of a market that is mid-cycle to late-cycle as depicted in Figure 1.

Figure 1 – Phases of the Credit Cycle

Our team expects these conditions to remain in the near term assuming the Strait of Hormuz is operating close to normal within the month. Macroeconomic conditions are decent, with economic growth expectations in the 2%-3% range. Inflation, while higher than the 2% target of the Fed, is manageable near 3%. Labor conditions remain a concern, given AI efficiency expectations, but for the time being unemployment at 4.3% is well below the long-term average. Additionally, wage growth is above its long-term average and slightly exceeds inflation.

We foresee top line growth for corporates to be in the high single digits in 2026. Technology companies will skew median figures higher, but we still expect ex-Mag 7 companies to deliver revenue growth in the mid-single digits. EBITDA margins are expected to remain stable in the mid-to-high teens, but risks are skewed to the downside provided higher energy prices. We expect companies to increase capital spending to take advantage of the accelerated depreciation tax policies of the One Big Beautiful Bill. While increased capital expenditures should lead to reduced free cash flow, outside of the hyperscalers we expect corporates in general to fund these efforts internally. That suggests that leverage should remain stable and supportive of credit quality. But what about the two flies in the corporate ointment – Energy and Private Credit?

Energy – Benign or Problematic Depending on Duration of Closure

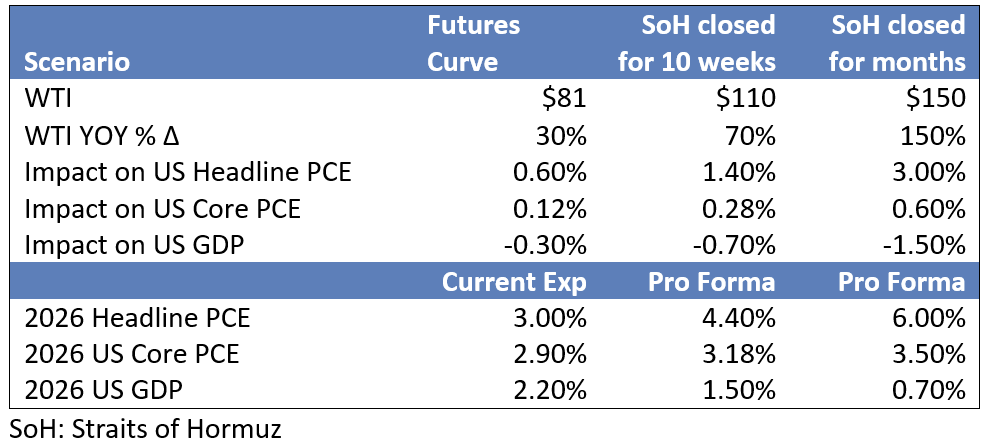

The closure of the Strait of Hormuz has been an energy supply shock that in the last five weeks has contributed to increased prices of crude oil (+40%), gasoline (+37%), diesel (+57%) and European natural gas (+47%). Depending on the duration of the closure, the impact of these price increases on inflation and economic growth ranges from modest to significantly problematic.

Figure 2 presents three scenarios we are using to help us assess fundamentals for the remainder of the year:

- The first is using the actual Nymex crude futures market (presently averages $81 per barrel for all of 2026); economic conditions are benign in this scenario and supportive of corporate credit quality.

- The second assumes the Strait of Hormuz is closed through mid-May and oil averages $110 per barrel for 2026; economic conditions are weak in this scenario and corporate fundamentals would likely deteriorate.

- The third assumes the Strait of Hormuz is closed for several months and oil averages $150 per barrel for 2026; economic conditions are near stagflationary in this scenario and we expect credit cycle factors would be flashing recession.

Figure 2 – Economic Scenarios Analysis Using Different Oil Price Scenarios

Drilling down from the macro to the micro, perhaps no sector is more influenced by the energy industry than the chemical sector. High oil prices are creating winners and losers across the industry. Somewhat ironically, the biggest beneficiaries are US-based chemical companies. U.S. companies primarily using natural gas as a feedstock, while areas like China and Europe rely on naphtha, an oil derivative. This “ethane advantage” has benefited US-based producers for years, but the gas-oil gap has widened substantially since the onset of the Iran war.

In addition, competitors in the Middle East that use natural gas cannot export products through the Strait of Hormuz. As an example, in the polyethylene chain, the conflict is impacting roughly 30% of global capacity. In response to a tighter global market and a steeper global cost curve, US polyethylene producers have announced the two largest polyethylene price increases ever in the US market.

While the conflict is currently creating a reprieve for domestic producers, the longer-term supply/demand imbalance that has existed for several years has not been solved and will return once the conflict ends. There is the added risk that the war results in demand destruction, which would make the situation even worse.

A similar dynamic has been unfolding in the fertilizer industry, particularly with nitrogen-based fertilizers. Compared to a year ago, domestic ammonia prices are 35%-40% higher, and granular urea prices are 60%-70% higher. North American-based companies are expected to benefit from this disruption.

Private Credit, Redemptions and Financials – Challenges Yes, Contagion No

The most immediate pressure point in the financial sector is retail wealth exposure, particularly in perpetual vehicles such as non-traded BDCs and interval funds. Recent redemption activity has made clear that permanent capital is not all the same — retail investors remain sentiment-driven rather than structurally committed. Redemption rates across perpetual BDCs with investment-grade debt averaged 1.6% of NAV through most of 2024, rising to 4.5% by 4Q25 and accelerating further to 5.7% in 1Q26, with several vehicles seeing requests materially above the standard 5% quarterly cap1. While redemption gates help contain near-term outflows, sustained pressure, particularly when concentrated among larger holders, signals potential structural fragility in the investor base. If elevated redemptions coincide with slowing inflows, previously stable capital and liquidity positions can erode over time, forcing reduced deployment activity, greater reliance on credit facilities, or asset sales.

The second-order effect matters most to the managers behind these vehicles: BDC redemption pressure flows directly into management company fee revenue, making wealth AUM concentration the key transmission channel, particularly if redemption activity spreads to other gated retail products. That exposure varies meaningfully across the alternative asset manager peer group, from approximately 31% at Blue Owl to roughly 3% at Brookfield2, and we expect it to be a key underpinning of earnings dispersion across the sector in the coming quarters.

Credit quality adds a second layer of risk across two channels. The first is software exposure in direct lending, where concentration is higher than platform-level figures suggest. Barclays estimates approximately 22% software exposure across BDCs with unsecured bonds, reflecting the weighting of software-heavy sponsor finance in these vehicles3. This exposure has taken on added significance as AI-driven disruption pressures software business models, a risk the market began repricing in early 2026, with a 2028 refinancing wall a further vulnerability where weaker fundamentals could crystallize losses not yet reflected in marks. Across the broader BDC portfolio, leading indicators are also deteriorating. JPMorgan’s fourth quarter BDC Quarterly Earnings Review flags two converging signals: average gross PIK as a percentage of net investment income was 15.6%, down 23 basis points year over year but up 119 basis points quarter over quarter, with 22 of 29 BDCs increasing sequentially; and non-accruals at cost rose to 2.05%, above the three-year average of 1.6%, with 19 of 29 BDCs moving higher4.

A separate but related risk sits in asset-backed finance, a market structurally distinct from corporate lending and largely the domain of alternative asset managers, with limited involvement from traditional managers. The market has grown to an estimated $6.1 trillion globally and is projected to reach $9 trillion by 20295, but several high-profile collateral integrity failures, including Tricolor, Market Financial Solutions, First Brands, and Broadband Telecom and Bridgevoice, where collateral is alleged to have been fabricated outright, suggest that underwriting and verification infrastructure has not kept pace with the speed of deployment in certain segments6. Unlike the gradual deterioration visible in BDC indicators, these failures are discrete and difficult to anticipate, and their emergence at scale raises questions about whether current marks across the asset class adequately reflect collateral risk.

Against this backdrop, the question for the financial sector is whether balance sheets have sufficient buffers to absorb these pressures before they become something more serious. For most alternative asset managers, the answer is yes: light leverage, strong liquidity, and recurring fee cash flows keep this in the category of earnings headwind rather than balance sheet stress, though that distinction is more comfortable for some managers than others. The more acute concern is whether sustained redemption pressure could compel managers to infuse capital into their BDC vehicles to stabilize investor sentiment, creating a transmission mechanism from BDC stress to manager balance sheets that are worth monitoring even where individual balance sheets look adequate today. That said, the picture is not uniform across the peer group. Managers with high wealth AUM concentration, high credit AUM concentration, and weaker balance sheet flexibility are more vulnerable to a scenario in which current conditions persist or worsen, and we expect these characteristics to be increasingly reflected in earnings and credit differentiation across the sector in the coming quarters.

From an insurance perspective, the transmission mechanism differs structurally from the redemption pressures observed in BDCs and retail wealth vehicles. Despite the growth in private debt in investment portfolios, management teams have consistently reiterated that their books consist of much more traditional allocations, such as investment-grade private placements, infrastructure, and 144A securities, rather than middle-market direct origination and leveraged lending, which are more aligned with how investors currently think about private credit risk (figure 3). Direct lending exposures, particularly to software, are measured in basis points of investment allocation for most insurers. BDC exposure is de minimis and limited to debt tranches rather than equity, meaning the retail redemption dynamics described above have minimal direct balance sheet impact.

Figure 3

More importantly, the liquidity risk at the center of the BDC concern is precisely where insurers have a natural structural advantage: annuity liabilities are long-duration and sticky, backed by surrender charge schedules that penalize early withdrawal, tax consequences that discourage it, and ALM frameworks purpose-built to match illiquid assets against illiquid liabilities. Surrender dynamics reinforce this; surrenders have come down from rate-driven peaks and are expected to decline further this year, reflecting more favorable policyholder behavior, and AM Best expects year-end 2025 statutory statements to show a record level of annuity reserves under surrender charge protection. This stands in stark contrast to the portion of private credit now funded by retail capital, where structural misalignment between funding needs and redemption expectations creates the fragility outlined above. From a rate perspective, while higher-for-longer rates pressure floating-rate borrower coverage ratios, life insurers are net beneficiaries on the liability side, earning higher new-money spreads even as they monitor credit deterioration in underlying portfolios.

That said, the tail risk worth monitoring is not a liquidity run in the traditional sense but rather a credit-loss feedback loop: if realized losses in private credit, particularly in more opaque subcategories like affiliated structured credit and direct lending are severe enough to impair an insurer’s financial strength ratings or risk-based capital, that could trigger policyholder surrenders and rating agency downgrades in a self-reinforcing cycle. This remains a low-probability scenario given that most private credit held by life insurers is investment grade and capital buffers are broadly adequate, but it is the right risk to underwrite rather than the retail-redemption dynamic that dominates the alternative manager narrative. Private credit remains something of a black box, where external parties cannot fully assess the risk of private letter-rated securities, and the growth of structures like rated note feeders adds further complexity. These concerns have drawn increased scrutiny from the NAIC and the US Treasury, which are meeting to discuss private credit risks. Improved disclosure and time remain the keys to sentiment recovery in the sector.

1 Barclays Credit Research, “Business Development Companies (BDCs): Declining in Flow Motion,” 6 April 2026.

2 Brookfield Asset Management Ltd. (NYSE: BAM), the listed asset management entity, distinct from Brookfield Corporation (NYSE: BN). Blue Owl Capital, investor presentation, February 2026; RBC Capital Markets, “Alternative Asset Managers Initiation,” February 23, 2026.

3 Barclays Credit Research, “Business Development Companies (BDCs): Widespread Exposure to Software Creates Uncertainty,” 2 February 2026.

4 J.P. Morgan North America Credit Research, “BDC Quarterly Earnings Review: BDC 4Q’25 Wrap Up,” 6 April 2026.

5 Integer Advisors and KKR Credit, as cited in “ABF Boomed in 2025 and Growth Is Set to Accelerate Next Year,” Private Debt Investor, December 30, 2025, https://www.privatedebtinvestor.com/abf-boomed-in-2025-growth-to-accelerate-next-year/

6 See: U.S. v. Chu et al., Indictment (S.D.N.Y. Dec. 2025) (Tricolor); U.S. Dep’t of Justice / IRS Criminal Investigation, “First Brands Executives Charged with Multibillion-Dollar Fraud” (Jan. 29, 2026), https://www.irs.gov/compliance/criminal-investigation/first-brands-executives-charged-with-multibillion-dollar-fraud; Bloomberg, “BlackRock Ensnared by Loans Tied to Firms Now Accused of Fraud” (Oct. 30, 2025) (Broadband Telecom/Bridgevoice); Financial Institutions News, “Property Lender Market Financial Solutions Enters Into Administration Amid Fraud Allegations” (Mar. 3, 2026), https://www.financialinstitutionsnews.com/2026/03/03/property-lender-market-financial-solutions-enters-into-administration-amid-fraud-allegations/.

Corporate Fundamentals 2Q26; AI Debt Issuance Can’t Stop Won’t Stop

July 16, 2026