Market Recap

By Tim Senechalle, CFA

Positive market momentum continued in the fourth quarter and contributed to healthy 2025 total returns across fixed income and equity markets. Corporate earnings growth, stable credit fundamentals, Federal Reserve rate cuts, and steady demand supported gains and valuations at historically elevated levels.

While positive multi-year trends continued in technology shares, precious metals and BBB quality credit, we note improved performance breadth with non-US equities, small capitalization companies, and Agency RMBS gaining greater favor.

Operating results for insurance companies will reflect the positive market backdrop with P&C industry book value gains from equity appreciation, and Life/Annuity sales are supported by attractive fixed rates in public and private market segments. All companies benefited from the credit backdrop with few incidents of default and new money reinvestment yields that continue to be meaningfully above run-off book yield levels.

Economic View

By Marco Bravo, CFA

Growth, the Treasury Curve, and the Fed

Our outlook continues to center on trend‑like U.S. growth with recession risks remaining low, supported by resilient consumer spending and improving business investment. Financial conditions are easing, household balance sheets remain relatively strong, and capital spending, particularly in AI, is providing an incremental lift. Against this backdrop, inflation continues to moderate but remains sticky, keeping the Federal Reserve cautious. We expect short‑term rates to move lower as the Fed delivers gradual easing, while long‑term Treasury yields remain range‑bound due to persistent inflation pressures and heavy deficit financing needs. This dynamic should drive a modest re‑steepening of the yield curve as policy rates decline faster than longer‑dated yields.

Our 2026 Outlook

Looking ahead to 2026, we expect GDP growth to align with consensus expectations near 2%, with consumption remaining the primary driver, led by middle‑ and higher‑income households. Inflation should continue to decelerate as shelter costs ease and demand normalizes, but is likely to remain above the Fed’s 2% target due to tariff pass‑throughs and tighter immigration policies supporting wage growth. In response, the Fed is likely to cut rates gradually, potentially two to three 25‑basis‑point moves, bringing the fed funds rate closer to 3% by year‑end, still restrictive by historical standards. Long‑term rates are expected to remain elevated, with the 10‑year Treasury ending the year near 4%, reinforcing a higher‑for‑longer environment even as policy becomes incrementally more accommodative.

Fixed Income Market

By Elizabeth Henderson, CFA

Investment grade fixed income delivered a strong year, with high single digit total returns and positive excess returns versus Treasuries. RMBS securities largely outperformed as prepayments remained low and OAS compressed. Corporate spreads ended largely unchanged, as BBBs and Financials outperformed and Technology and Communications underperformed due to AI-related supply surprising to the upside and fallen angels in Media. Rating activity remained positive, reflecting healthy fundamentals. Intermediate bonds outperformed long, as CMBS and ABS posted more modest gains. Municipals also outperformed on strong technicals, as tax-exempt supply came in well below expectations and reinvestment demand stayed favorable heading into 2026, though taxable municipal spreads widened slightly despite solid demand. This presented opportunities in the University segment of the Taxable market.

AAM Fixed Income Performance

By Elizabeth Henderson, CFA

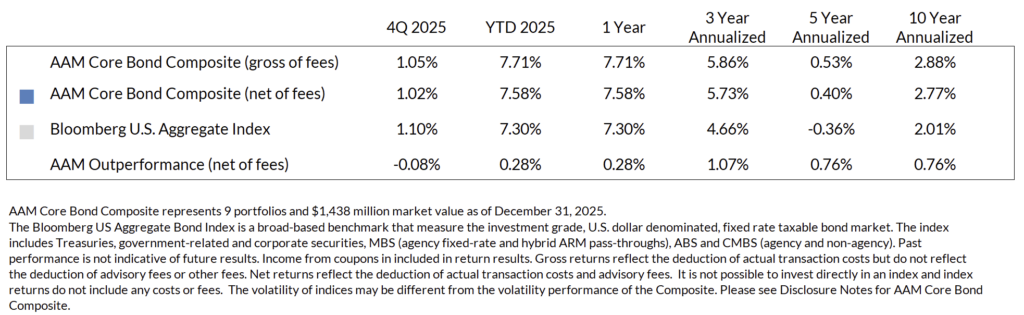

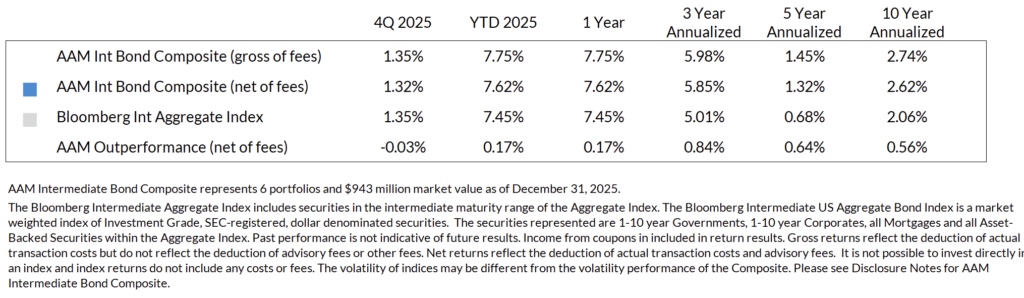

AAM’s Core and Intermediate composites outperformed their benchmarks in 2025, driven by a balanced combination of a strategic underweight to Treasuries, which lagged spread sectors, and strong security selection. Tactical adjustments added value, including increased allocations to current coupon mortgages, corporate bonds, and CMBS, alongside reduced exposure to CLOs and U.S. Treasuries. Security selection was a notable contributor across the curve, particularly in RMBS (nonagency and current coupon), ABS (esoteric and rate reduction, new issues), corporate bonds (new issues, cyclical and financial issuers), and taxable municipals (new issue universities). While AAM’s defensive long end corporate positioning created some drag amid historically rich spreads, this was offset by outperformance in taxable municipals, and enhanced short end income also contributed positively to total returns.

AAM Core Bond Composite

AAM Intermediate Bond Composite

Outlook for Insurance Portfolios

Public Fixed Income: Stable, Selective, and Valuation‑Constrained

The 2026 outlook across investment‑grade corporates, structured products, and municipal markets is broadly stable but increasingly selective, with modest return expectations and a greater emphasis on credit quality and sector dispersion. With risk premia narrow across public markets, returns will be driven less by beta and more by security selection and access to primary issuance.

Corporate spreads are expected to widen modestly as technical tailwinds fade from historically strong levels. Increased supply tied to M&A and AI investment, the potential for reduced foreign demand for USD‑denominated fixed income, and late‑cycle fundamental pressures all argue for a more cautious stance. Within this environment, stronger fundamentals and relative value favor Banks and Utilities, while Technology sectors could see spread pressure and potential rating challenges stemming from elevated AI‑related capital spending.

Structured products, which outperformed in 2025, are expected to do so again in 2026, supported by strong technicals—particularly in Agency MBS as GSE demand remains firm and housing affordability reforms gain traction. CMBS and ABS continue to offer attractive spread premiums versus Treasuries, though refinancing risk remains a concern in office‑heavy CMBS collateral. Diversified pools present opportunity, while CLOs may lag amid falling policy rates and elevated issuance. Selection across collateral and structure will be increasingly important.

In municipals, elevated supply and rich valuations make tax‑exempt bonds less compelling for institutional buyers. By contrast, taxable municipals offer more favorable spreads alongside stable credit fundamentals, with higher education issuers in particular demonstrating resilience. As in other sectors, consistent access to the new‑issue market will be critical for improving relative value and flexibility.

Expanding Beyond Public Markets: Opportunities and Risks

With public market spreads tight, insurance companies continue to expand allocations to non‑public market segments where additional yield can be earned through liquidity, structural complexity, or underwriting expertise. Commercial real estate lending and AI‑related infrastructure project finance remain areas of opportunity, though outcomes will increasingly be differentiated by the rigor of upfront underwriting and structuring discipline.

Non‑public markets continue to attract regulatory and political scrutiny, warranting careful consideration when deploying capital in lower‑liquidity strategies. While many regulatory changes are well telegraphed, they could still pressure select segments of private markets where insurers are forced to sell illiquid assets in response to unfavorable capital treatment.

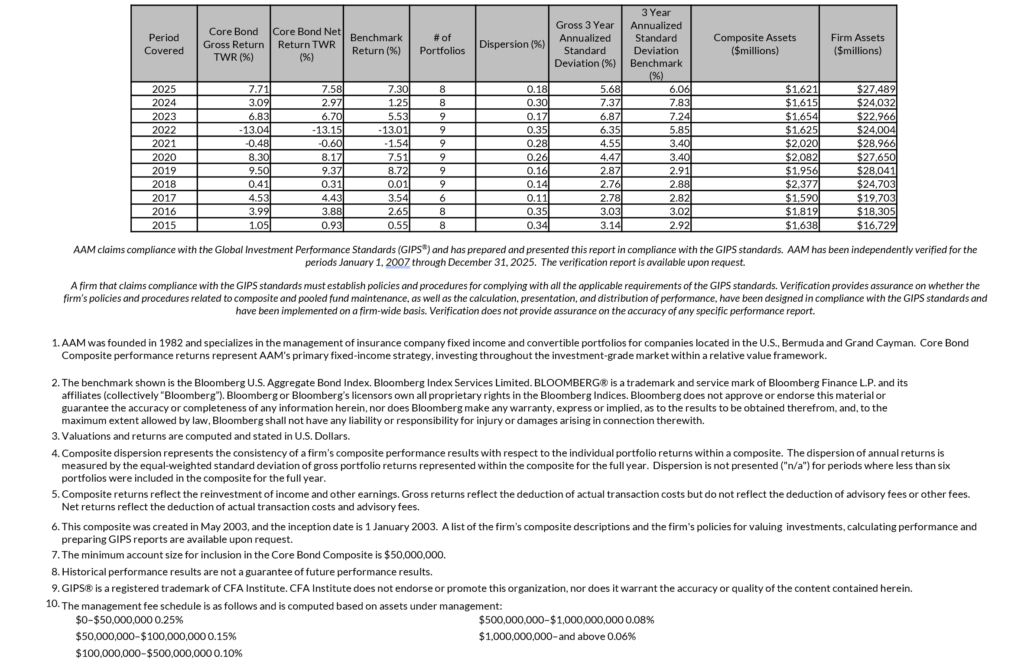

AAM Core Bond Disclosure Notes

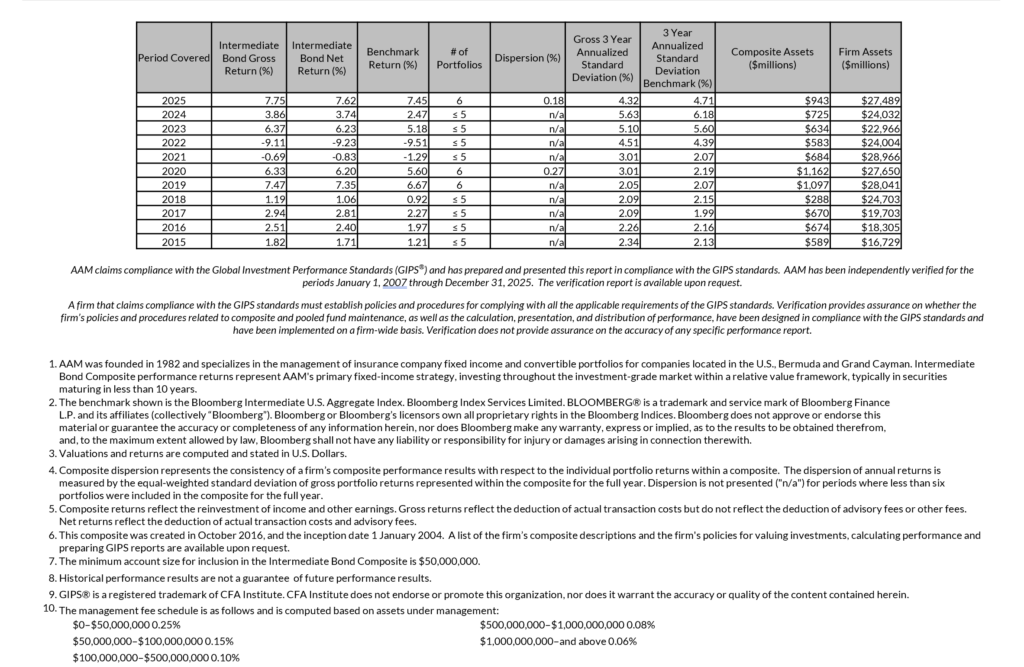

AAM Intermediate Bond Disclosure Notes

Corporate Fundamentals 2Q26; AI Debt Issuance Can’t Stop Won’t Stop

July 16, 2026