Fixed Income Summary

By Elizabeth Henderson, CFA

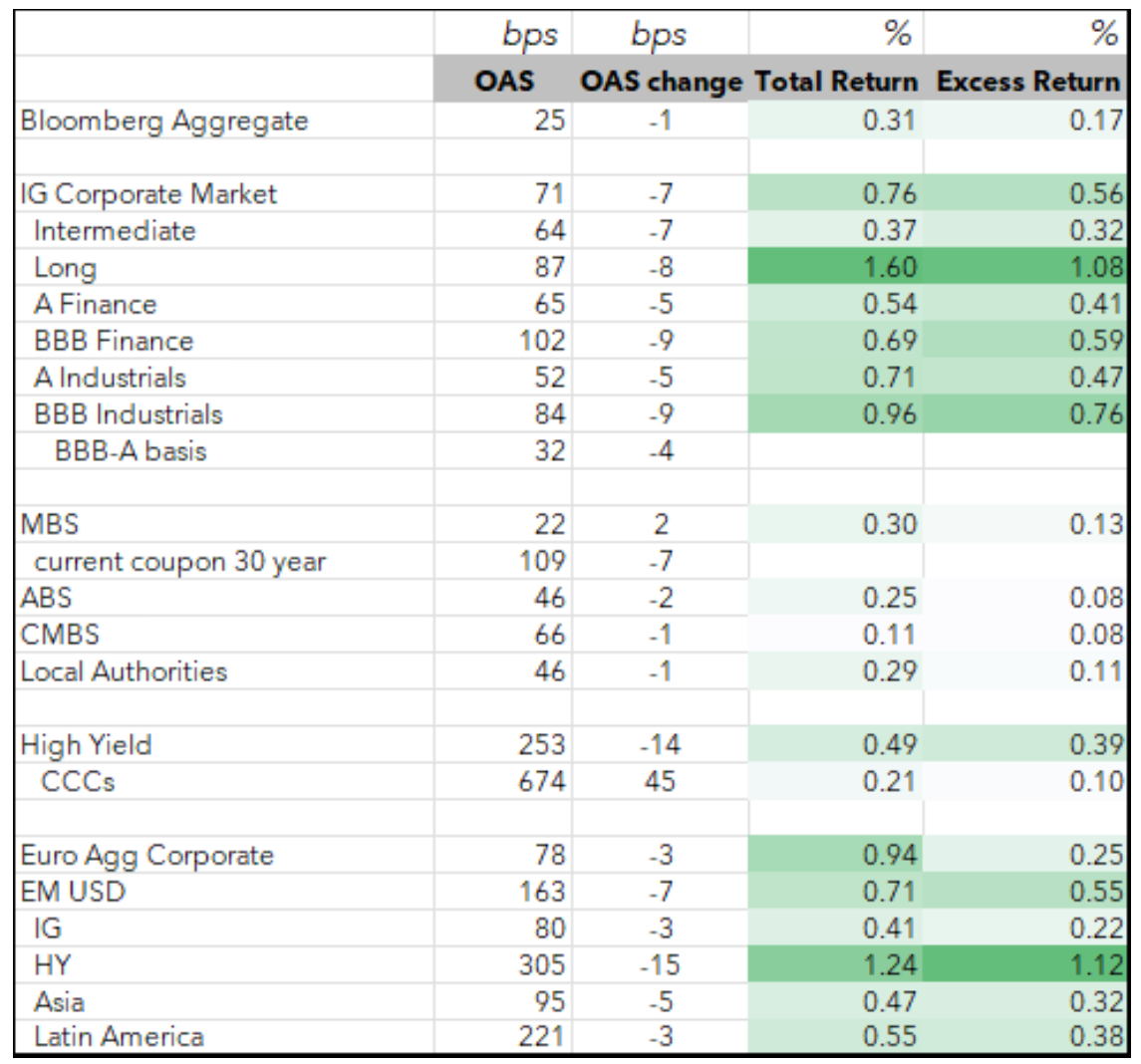

Investment grade fixed income delivered broad-based positive excess returns in May as spreads tightened across corporates, structured products, and municipals despite a weakening Treasury market. IG corporate spreads closed the month within 1 bp of multi-decade tights, supported by strong first-quarter earnings and robust trading volumes. Structured sectors followed suit, as Agency RMBS produced +13 bps of excess return, CMBS absorbed its heaviest issuance month of the year, and ABS supply surged. Taxable municipal spreads tightened across most of the curve, while tax-exempt municipals materially outperformed Treasuries as mutual fund flows and reinvestment demand strengthened heading into summer. The constructive tone was underpinned by declining volatility, favorable technicals, and solid fundamentals, though geopolitical risks tied to Iran, historically tight valuations, and a projected pickup in June supply across most sectors argue for measured positioning heading into the second half of the year.

IG Fixed Income Recap

Corporate Market

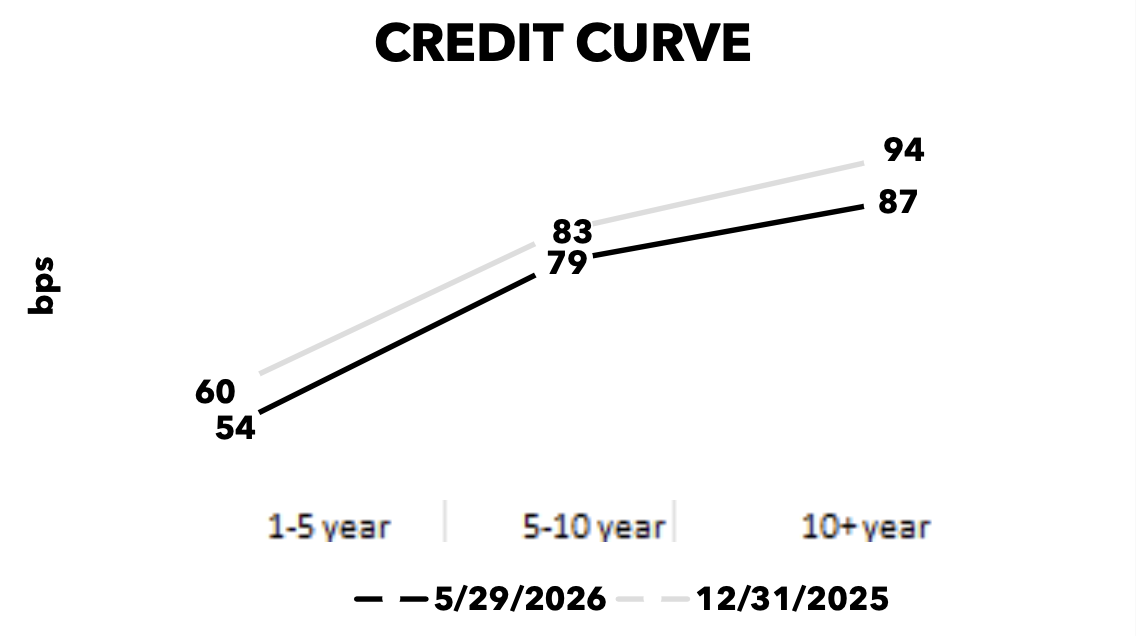

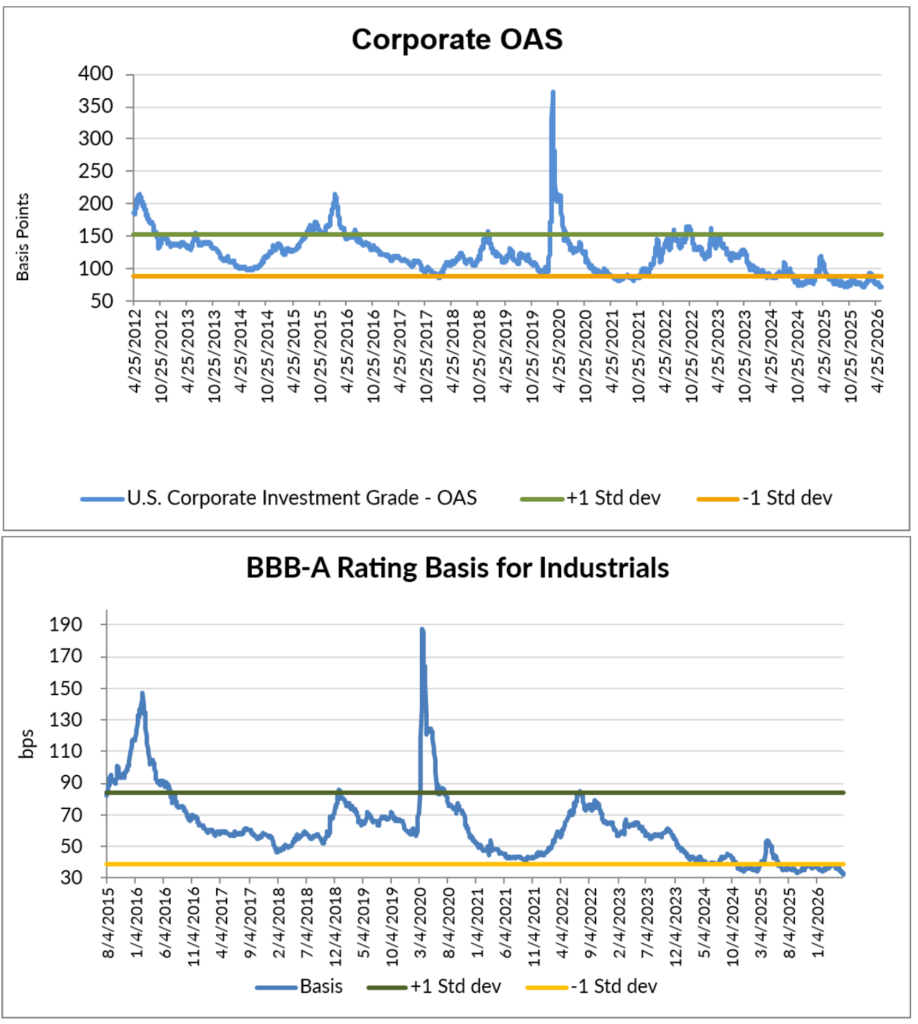

IG spreads ground tighter throughout May, moving from +79 on May 1 to +72 by month-end, a 7bp tightening that brought the index within 1bp of the multi-decade tights. 1Q’26 corporate earnings were very strong for both non-cyclical and cyclical firms. Fundamentals remained solid, though cash balances declined and net leverage ticked higher. BBB-rated Industrials outperformed, with spreads at historic tights. The pick-up in spread for ‘BBB’ vs. ‘A’ rated Industrials is 32 bps, more than one standard deviation inside of the long-term average of 61 bps. Spreads on the long end (10+ year maturities) have also returned to their historic minimum levels, as investors seek higher yields and the supply of newly issued 30-year debt has fallen. The market is paying up for commodity and industrial cyclicals while demanding more spread in media, tech, and financials, a positioning that reflects confidence in the real economy but skepticism toward sectors facing structural headwinds and/or continued new issue supply.

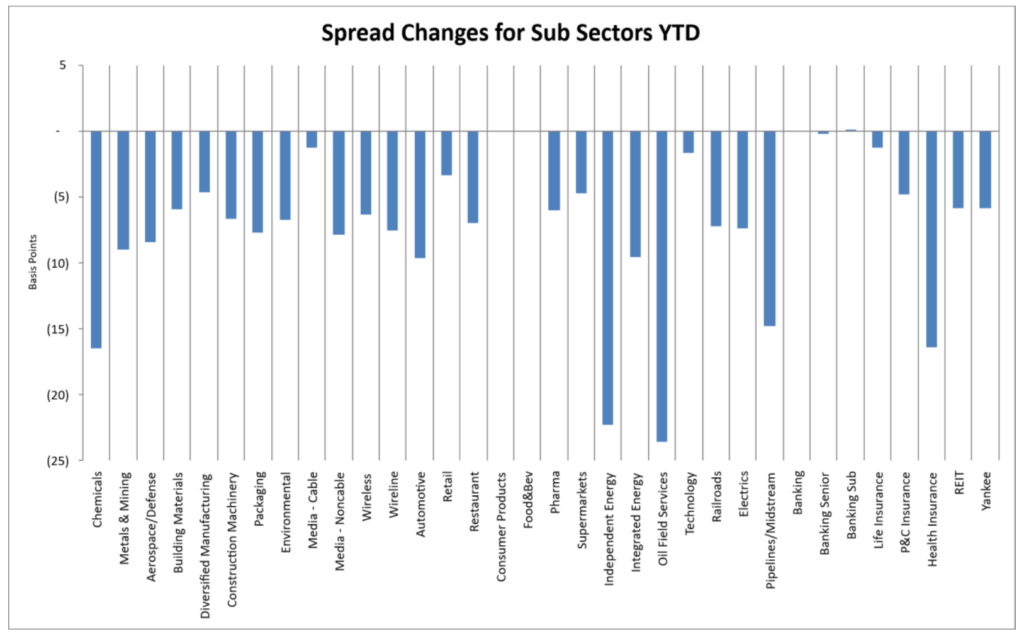

Looking at sectors relative to Industrials (Sector OAS/Industrial OAS):

Z scores >1.5: Cable, Technology, Finance Companies, Life Insurance, Supermarkets (LTM), Health Insurance (LTM)

• Z scores <-1.5: Metals & Mining, Environmental, Independent Energy, Midstream, Integrated Energy (LTM), Oil Field Services, Diversified Manufacturing, Construction Machinery (LTM), Aerospace & Defense, Railroads (LTM)

Source: Bloomberg, AAM (bold=new for the month; strike-through = no longer valid vs last month; 5+years unless noted for last twelve months)

Corporate Market Technicals and Rating Changes

June issuance is expected to slow to $120B, which is heavy historically for June but down from $164B in May. Issuance was less than expected in May after an active April. BofA expects new issue supply less coupon income to be negative in June. There is upside risk to this figure given rising commercial paper balances per JPM.

The average daily trading volume for HG bonds was $46.2B in May, about 21% higher vs. May 2025. YTD, trading volume is 14% higher. New issue supply was skewed toward front end and financials in May. Hyperscaler issuance moderated as issuers accessed other markets (CHF, JPY).

HG funds and ETFs had inflows in May with ETFs accounting for the majority of flows with more interest in short-and-intermediate strategies.

Sources: AAM, Wells, BofA

Rating changes this month (rising stars/fallen angels at unsecured level per Bloomberg)

- Fallen angels: none

- Rising stars: Teva, AngloGold Ashanti Plc

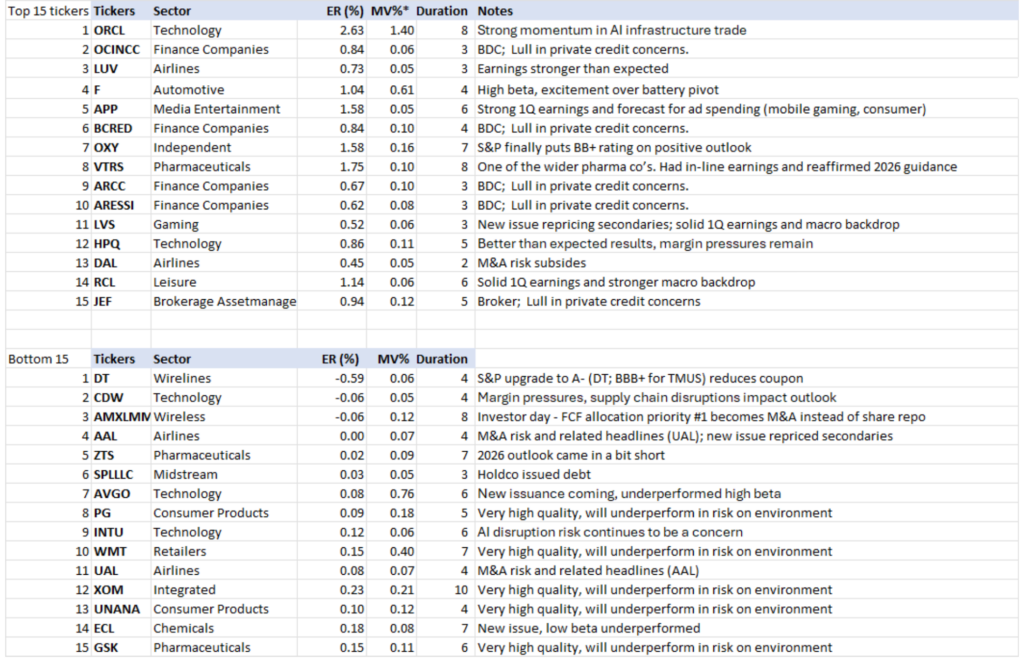

Ticker Level Performance

The following shows the top and bottom performing issuers based on ‘excess return per unit of duration’. This list excludes most with market values less than 0.05% of the Bloomberg Corporate Index as well as non-corporate issuers. AAM’s analysts have provided an explanation for issuer performance when relevant.

Corporate Market Graphs

(Source: Bloomberg, AAM)

Structured Products

By Chris Priebe and Mohammed Ahmed

Agency MBS outperformed slightly while CMBS and ABS also produced positive excess returns in May.

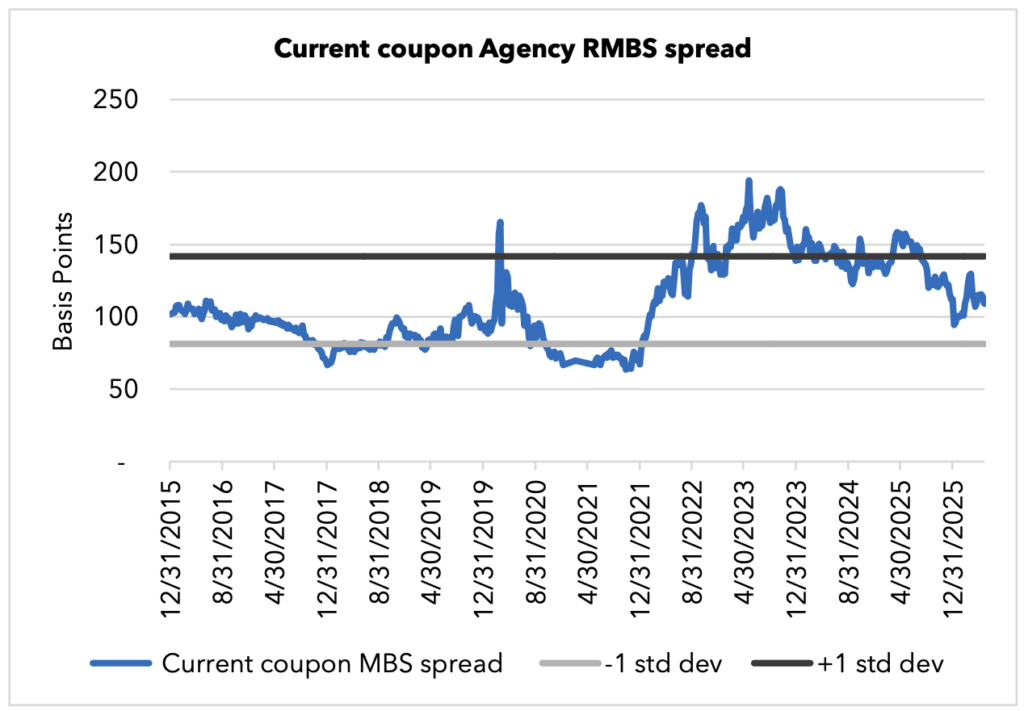

(Source for chart: Bloomberg – FNCL CC Spread to 5/10)

AGENCY RMBS Excess Return: +13 bps

Current coupon Agency RMBS posted a second consecutive month of positive excess returns as spreads tightened six basis points, opening near +114 and closing near +108, the lowest level since late December. Performance was mixed across coupons: deep discount 30-year 2.00s and premium 6.00s led with +18 and +23 bps respectively, while 2.50s and 3.00s lagged at +8 and +2 bps. Interest rate volatility, as measured by the MOVE Index, was unchanged in May. Low affordability given higher mortgage rates and subdued new home sales have kept net MBS supply in check, although hybrid ARM issuance is increasing. The National Home Price Appreciation slowed to 0.7%1.

CMBS Excess Return: +8 bps

Non-agency CMBS had its busiest month of 2026, with approximately $19.8B of transactions pricing in May, skewing toward 5-year conduit deals. Despite the heavy calendar, spreads remained range-bound in the high 70s with 3–4 bps of new issue concession. The market’s ability to absorb record supply at stable spread levels suggests continued strong technical demand. Broader CRE fundamentals are improving, and the office distress cycle is moving from delinquency into resolution. Refi rates around 68–73% suggest most maturities can be addressed, though office remains a weak outlier.

ABS Excess Return: +8 bps

The ABS sector had another busy month with $40 billion in supply pricing in May. Year-to-date issuance has reached close to $178 billion, up 24% from a year earlier. ABS produced 8 bps of excess return, led by autos at +9 bps, while cards and utilities each produced +5 bps. AAA CLO spreads tightened 5 bps on the month as LIBOR assumptions moved higher in the futures market. Consumer fundamentals underpinning the sector remain bifurcated: homeowners, especially those who purchased pre-2022, are materially stronger than renters and post-2022 buyers, while rising electricity and essential device payments are increasingly competing with traditional debt in the consumer payment waterfall.

1 S&P CoreLogic Case-Shiller

Municipal Bonds

By Greg Bell, CFA, CPA

Taxable muni spreads tightened across most of the curve in May, with demand strongest in the shorter end of the curve (<7 years). Tax-exempt munis outperformed Treasuries meaningfully, as fund flows surged, though significant issuance in June may temper further improvement in relative valuations.

Taxables

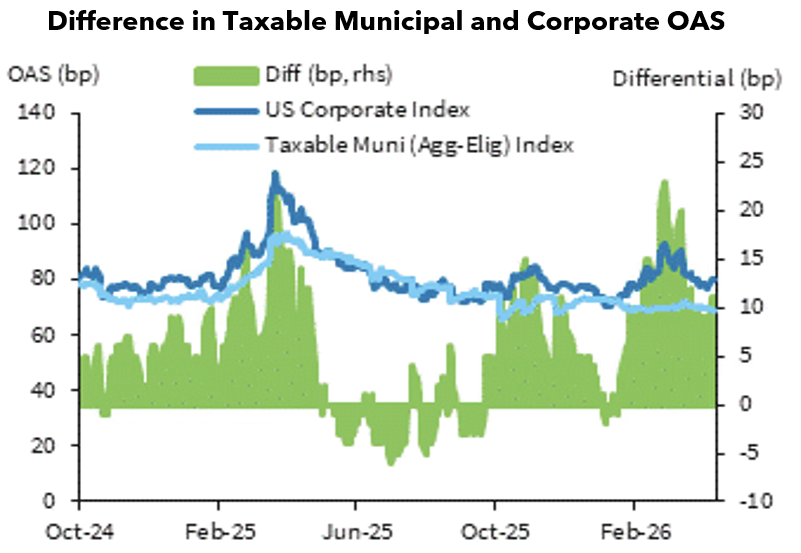

Spreads across the taxable municipal curve generally moved tighter during May, with the exception of the 5-year area, which was unchanged. Spreads in 3-, 7-, 10- and 30-year maturities tightened by 3, 5, 4 and 5bps, respectively, reflecting the resilience of institutional demand across the curve. (Source: Bloomberg, AAM)

The market continued to benefit from better demand flows in the higher rate environment and the elevated yields that have prevailed over the past two months. Supply remained muted and continues to provide an important catalyst for stabilized spread behavior amid the heightened market gyrations tied to Iran war developments. Demand was strongest in maturities of seven years and shorter, pushing spreads in that range to near five-year tights. (Source: AAM, Bloomberg, Morgan Stanley)

Although 10-year spreads moved tighter by 4bps, the spread pickup between 5- and 10-year maturities remains modestly wide at approximately 20bps, though through the long-term average of 25bps. The 10-year and longer area of the curve continues to provide a better area for investment relative to the short-intermediate portion of the curve, seven years and shorter. (Source: AAM, Bloomberg)

Looking ahead, the persistently muted new issue profile relative to the broader municipal market, combined with a stable underlying credit environment, should keep taxable spreads rangebound around current levels. Demand support is expected to remain most durable in the front and intermediate portions of the curve, even as the relative value case continues to favor the 10-year and longer area. Broader rate volatility tied to the ongoing geopolitical backdrop remains the key risk factor to spread stability in the near term. (Source: AAM, Bloomberg)

Tax-exempts

Favorable technicals provided the backdrop for stronger relative performance during May. Mutual fund flows surged during the final week of the month to $2.35B, contributing to a 242% increase in the four-week moving average from the end of April. The improvement in fund flows reinforced the constructive demand tone that had been building since the post-Tax Day recovery and proved sufficient to support tightening relative valuations through month-end. (Source: Lipper, Bond Buyer, Bloomberg)

That improvement in fund flows coincided with solid positive momentum in reinvestment flows from coupons, calls and maturities. May reinvestment flows were expected to increase approximately 51% over April’s pace, with June projected to rise another 42% to approximately $80B. The progressively stronger reinvestment profile provides a meaningfully larger demand offset heading into the summer months and underpins the improving technical backdrop for the sector. (Source: Bond Buyer, BofA)

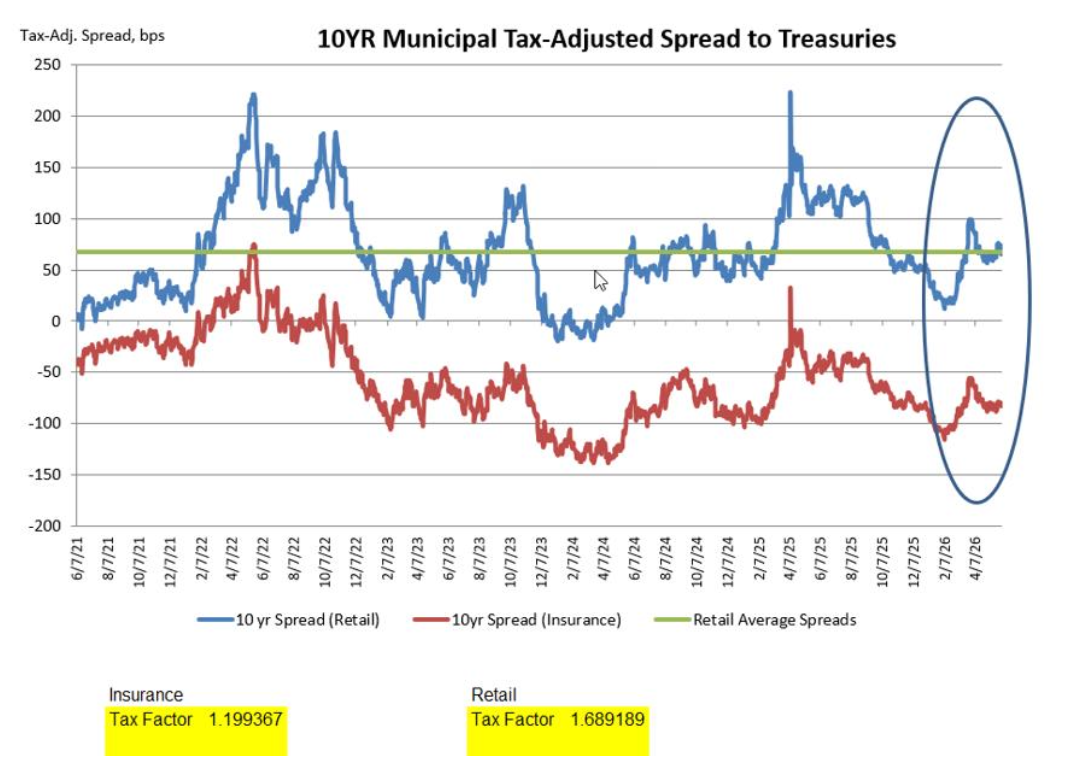

This improved technical profile allowed the tax-exempt sector to hold in very well against a weakening Treasury market. For the month, tax-exempt yields were unchanged in 3-year maturities and higher by a modest 2bps in 10-year maturities, in stark contrast to the 16 and 7bps moves higher in Treasuries over matching tenors. Relative valuations richened accordingly, with tax-adjusted spreads tightening by 16 and 4bps in 3- and 10-year tenors, respectively. (Source: Bloomberg, Refinitiv)

Offsetting these favorable demand technicals will be a continued surge in new issue supply. May issuance is expected to be reported at approximately $48B, while June is projected to be the largest issuance month of the year atapproximately $59B. The competing technical profile is expected to result in a more muted movement in relative valuations over the next month, as heavier supply absorbs a meaningful portion of the improving reinvestment and fund flow demand. (Source: Bond Buyer, BofA)

On a tax-adjusted basis, 10-year spreads to Treasuries ended the month at -86bps. For institutional investors subject to the 21% corporate tax rate, that level remains well below competing taxable alternatives, continuing to limit crossover demand for tax-exempt securities at current relative value levels. (Source: AAM, Bloomberg, Refinitiv)

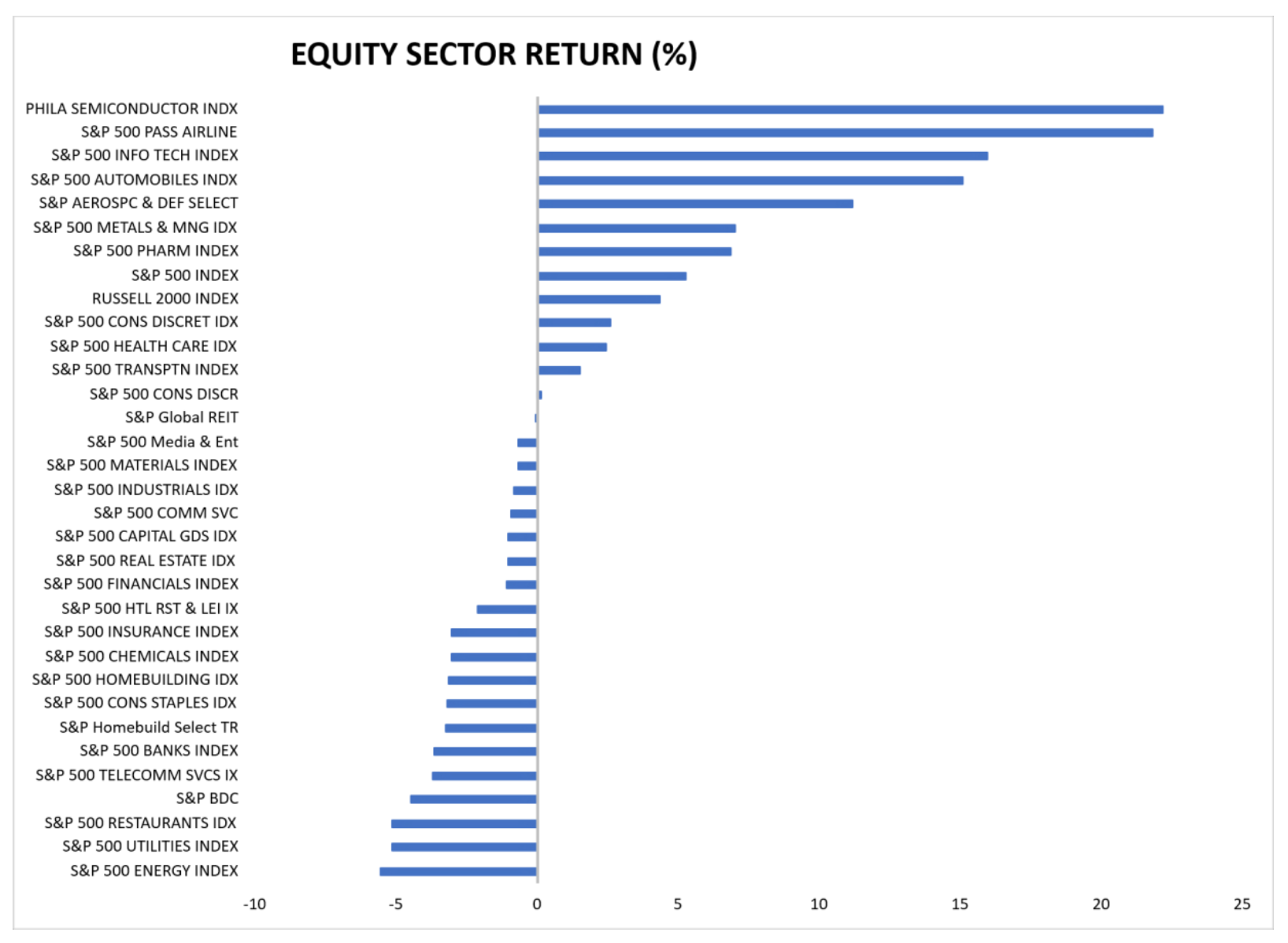

U.S. Equity Performance – May

End of the Line? The Fight Over America’s Great Rail Merger

July 8, 2026